(Please consider making even a small contribution to the Welcome to Pottersville2 Quarterly Fundraiser happening now ($5.00 is suggested for those on a tight budget) or sending a link to your friends if you think the subjects discussed here are worth publicizing. Thank you for your support. We really appreciate it. Anything you can do will make a huge difference in this blog's ability to survive in these difficult economic times.)

My computer died and I'm living off the charity of friends and the library.

I know you're not religiously inspired, but a few prayers to the computer fixit gods may be in order. Thanks for your aid and good thoughts.

From OpEd News:

John Jonik ( http://jonikcartoons.blogspot.com)

Why I’m Fed Up with Summers

By Jim Hightower

Will America ever get rid of Robert Rubin?

The Wall Streeter became a top economic witch doctor for Bill Clinton in the 1990s. During his tenure, he convinced old Gullible Bill toHeck of a job, Robbie!

Having worked his black magic with Bill, Rubin hightailed it back to Wall Street, where he led Citigroup into a bunch of reckless gambles, resulting in serial bailouts that cost us taxpayers hundreds of billions of dollars. But Rubin wasn’t through.

Among his protégés are Timmy Geithner and Larry Summers. He helped slip them into the top economic spots in the Obama regime.

Geithner, a true friend of Wall Street, led the Treasury during Obama’s first term in office. He dutifully fought such true reformers as Elizabeth Warren, when she was trying to stop the Street’s too-big-to-fail greedheads.

Summers, an economics professor fond of sticking his foot in his mouth, was the “genius” who convinced Obama in 2009 to implement only a small, weak stimulus plan, then to surrender even that to Republican demands for a failed, budget-butchering, austerity scheme.

With a record like that, surely we’ve heard the last of the Rubinistas, right? We wish! But, no.Astonishingly, Rubin’s deep circle of economic Hell has been pushing Larry “Screw-Up” Summers on Obama, saying he’s just the man to take over the Federal Reserve. For some reason, he’s supposed to steer America’s national monetary system and be trusted to fix our economy.

Sure he is. The problem is that for Rubin & Co., the word “fix” has the same meaning as it does for your veterinarian.

To say “no!” to Summers, go to TheNation.com/activism.

The ‘Bankization’ of America

By Richard (RJ) Eskow

The share of our national income, which goes to corporate profit, is the highest it’s been since they started tracking it in 1929, while the share going to people – as salary and wages – is the lowest. And the percentage of that corporate profit which goes to Wall Street is also the highest on record.

We’re becoming a financialized economy. Never before has the manipulation of money counted for so much and the real-world economy of people and consumer goods counted for so little.

And none of it is an accident.

When Wall Street catches a cold …

The Wall Street Journal reported this Thursday “Stock and bond prices tumbled after stronger-than-expected economic data …”

Why would good news about the economy cause the stock market to fall? The sentences continue: “… raised investor anxiety about a pullback next month in central-bank support for financial markets …”

Investors had been relying on the Federal Reserve to keep pumping up the stock market’s record run, but some mildly favorable economic reports raised fears were raised that the Fed’s market-friendly interventions might come to an end.

“We’re getting another knee-jerk reaction to fears of tapering,” a market analyst told the Journal, referring to the Fed’s monthly purchase of $85 billion in bonds. As Reuters reported last month, “Many on Wall Street believe the Federal Reserve’s monetary policy is behind record corporate earnings and the stock market’s surge to all-time highs this year.”

When Wall Street catches a cold – when it even might catch a cold — the economy catches pneumonia.

Reality Bites

Meanwhile, the “real” economy – the one where people live, and work, and buy things – has suffered even as Wall Street and the stock market have boomed. That trend continued this week too; Wal-Mart announced disappointing sales and lowered its projections. Its Chief Financial Officer observed, “The retail environment remains challenging in the U.S. and our international markets, as customers are cautious in their spending.”

Cisco also lowered its sales expectations. As the Journal article notes, these announcements added to the fear that the Fed’s interventions might wind down.

This stock market story illustrates the gulf between a stock-market economy increasingly driven by the banking industry – an economy which has been booming, today’s news notwithstanding – and a human economy wracked by consumer fears, falling wages, joblessness, and low-level jobs for a growing number of people who are working.

The gulf between these two economies drove this morning’s stock market story. It’s also driving the long-term depression-like misery, which holds millions of Americans in its grip.

This is not the playing out of some divinely decreed order. The financialization of the US economy is the result of very deliberate governmental choices. Unless different choices are made going forward, we will continue to become a “Bankistan” whose wealth and economic fate is increasingly hijacked by Wall Street.

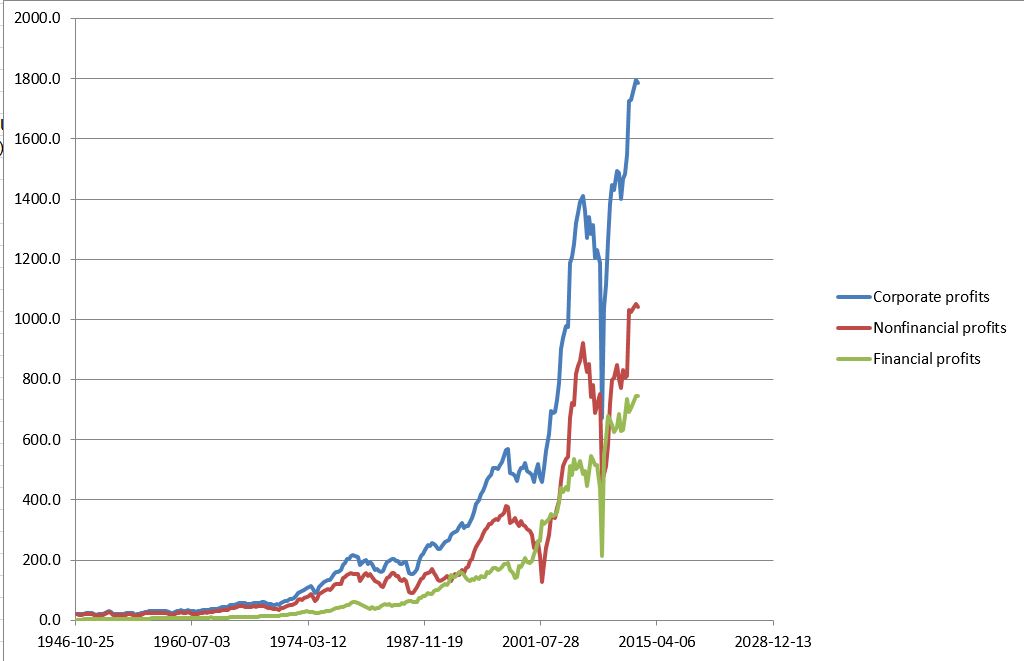

Financialized

The Federal Reserve’s data on corporate profits were helpfully compiled by a contributor to the investment site The Motley Fool, who notes that financial profits were 11 percent of total corporate profits in the US back in 1947, the first year these numbers were compiled.

These profits soared in the first decade of the 21st Century. After taking a hit in the crisis of 2008 – a crisis that the banking industry caused – they rose again and are now at record highs. Their share of total corporate profits has risen from 11 percent to 42 percent, as of the latest report, and the Fed expects them to keep rising.

Here’s how that looks:

The money nowadays isn’t in manufacturing, or retail, or any of the other traditionally jobs-producing industries. The money now is in money.

How did this happen?

A series of policy decisions enabled this explosive growth, including the deregulation of Wall Street; the repeal of Glass-Steagall, which separated bank customers’ money from money which the bank could invest for its own profit; runaway banker salaries and bonuses, which prompted the “best and the brightest” to flock to Wall Street and apply their ingenuity to flouting the rules; and government’s increasing unwillingness to indict bankers for criminal behavior.

And then, when banker criminality and incompetence created the crisis of 2008, the government rescued them without being held financially or legally accountable for their wrongdoing.

The Federal Reserve continues to pursue stimulus policies that moderately help the economy as a whole, but which emphasize the economic health of banks and publicly traded corporations over that of companies that hire workers – and therefore increase the consumption of consumer goods.

Profit by the slice …

Banks have a bigger share of the corporate-profit pie – and that pie’s bigger than ever. As Floyd Norris notes in the New York Times, the government’s revised estimate of wage and salary income is 42.6 percent of GDP, which matches the 2010 figure as the lowest percentage since this data was first captured in 1929.

Using the latest revisions to the national income and product account (NIPA) data produced by the Bureau of Economic Analysis, Norris also notes that corporate profits are now 9.6 percent of GDP. That’s the highest since these figures were first captured.

As Norris also notes, corporate taxes rose slightly in 2012 as a percentage of GDP but are still well below their historical averages. That’s not an accident either.

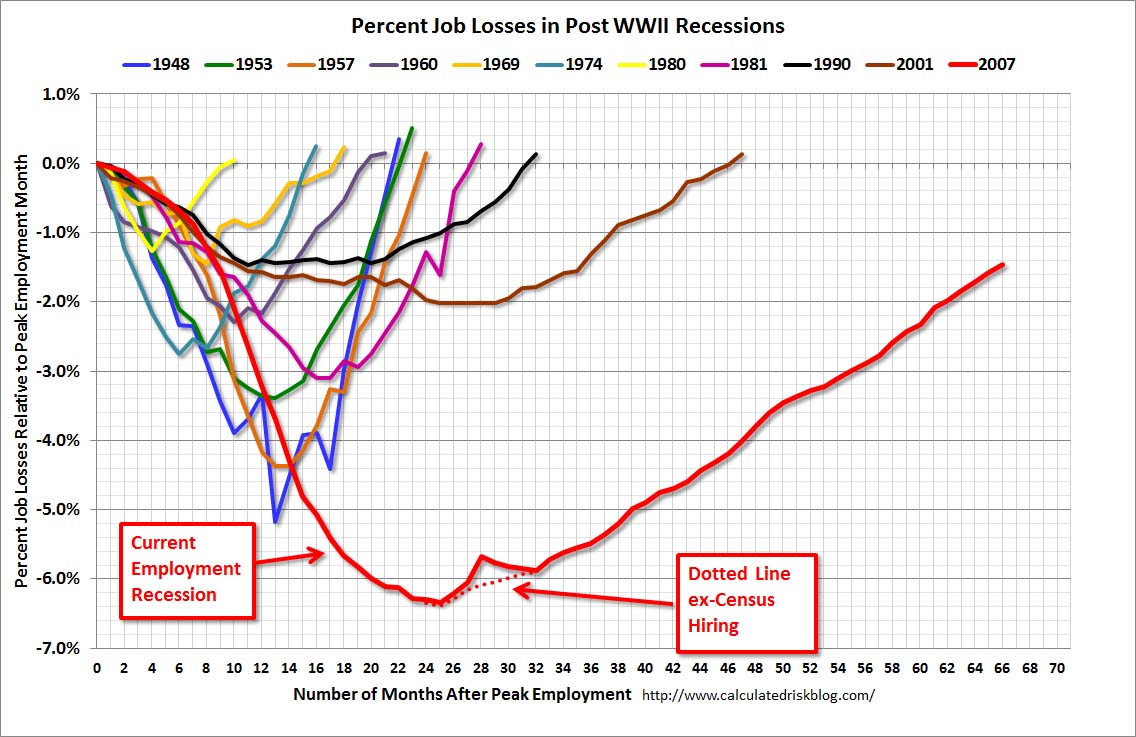

Meanwhile, as this chart shows, unemployment remains horrendous:

(via Bill McBride, Calculated Risk)

Wages actually fell for most people after the 2008 crisis, as high-income individuals (the top 1 percent) captured all of the economic gains created by the government-sponsored recovery – and even enlarged their share, capturing 121 percent of the recovery as the rest of the country fell behind.

Indebted

You might think that financial institutions feel indebted to the public for rescuing them. But the opposite is true: We’re indebted to them. According to the latest report from the New York Federal Reserve, auto loan balances increased by $20 billion over the previous quarter while credit card balances and student loan debt increased by $8 billion each.

The falling rates of mortgage debt, driven by range of factors which included falling housing values and foreclosures, resulted in an overall decline in total indebtedness. But these figures show that our household debt in many key areas continues to rise.

As wages and salaries decline, people are struggling to keep up with the way of life they once know. So they fall deeper in debt – a debt that allows them, and the banks, to delay the day of reckoning once again.

Fixing a Hole

These figures paint the picture of an economy that has become seriously unbalanced in favor of the banks – “financialized,” as observers increasingly describe it. How can the economy be rebalanced?

Many solutions are well known to bank reformers and well-informed voters: Reinstate Glass-Steagall, or something very much like it. Insist on strong regulatory oversight of the banking sector, and give regulators the authority to do their jobs. End “too big to fail” banks, instead of encouraging their consolidation (as the government has done in recent years).

Prosecute criminal bankers.

Other solutions are equally important. The interbank database and shell company called MERS must be ended, so that financial institutions can’t collude against consumers and the states. The Federal Reserve must demand that banks perform their central economic function – responsible lending to consumers and job-creating businesses – rather than reward them for speculation and other forms of non-productive profiteering.

(That’s why the choice of Federal Reserve head is so important.)

Genuine shareholder reform is also needed, so bankers don’t overpay themselves at shareholder expense or use the bank’s coffers as a “get out of jail” card for massive settlements caused by their own misdeeds.

Lastly, no comprehensive solution can be found until banks and other corporations are once again taxed at reasonable levels and the revenues are used to create well-paying jobs for the American middle class.

A healthy economy needs banks that lend, and consumers with the money to buy. Until that happens we’ll be living in a highly financialized “Bankistan” that excludes most of its citizens from sharing in the American dream.

No comments:

Post a Comment