(Brendan McDermid | Reuters)Traders on the floor of the New York Stock Exchange.

The selloff in U.S. equities continued on Monday as the S&P 500 closed in a correction and the Dow Jones industrial average ended nearly 600 points in the red.

Check out some of the stats here:

- Monday ended the biggest three-day loss for the Dow ever with 1,477.45 points shed. (The next biggest three-day loss for the Dow totaled 929.49 points in November 2008.)

- The Dow has been down five consecutive days for a point loss of 1,673.9.

- Cumulative volume traded was 13.94 billion shares for the highest volume day since Aug. 10, 2011, when 15.19 billion shares traded.

- The Dow traveled more than 3,000 points within the first 90 minutes of trading on Monday.

- WTI settled down 5.5 percent for the worst day since July 6 when it lost 7.73 percent. (Monday's low of $37.75 was WTI's lowest point since Feb. 24, 2009, when it hit a low of $37.65.)

- 9 out of 10 S&P 500 sectors are in correction; (energy and materials are off their highs by 20 percent or greater).

- Industrials, tech, telecom, utilities, financials, consumer discretionary and health care are all of their highs by 10 percent or more.

- S&P 500 companies collectively lost about $685 billion in market cap (about $100 billion more than Apple's market cap).

- NYSE volume was at 6.57 billion shares, the heaviest since Oct. 27, 2011.

Remember the Christmas card featuring the rich guy playing tennis in his ornate living room with his family?

They're back.

And looking for another handout soon.

Markets Dive: Keep Your Eyes on Wall Street Bank Stocks

By Pam Martens and Russ Martens

August 24, 2015

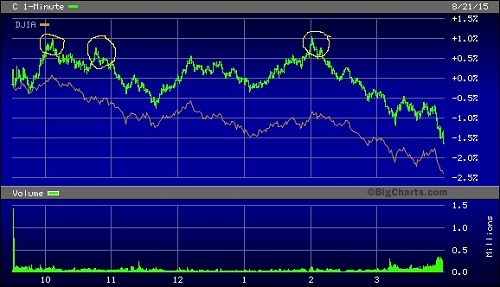

Trading in Citigroup (Green) Versus Dow Jones Industrial Average (Orange)

Friday, August 21, 2015

After an 8.5 percent plunge in China’s Shanghai Composite Index on Monday (bringing its loss for the month to a negative 21 percent), a drop in the U.S. Dollar and the U.S. crude oil benchmark, West Texas Intermediate, slipping below $39 a barrel, futures on the Dow Jones Industrial Average at 8:27 a.m. are flashing an ugly opening in New York, with a potential loss of as much as 648 points. (That could materially change before the market opens at 9:30 a.m.)

Mainstream media seem obsessed with what actions the central bank of China might take to stem the rout while also focused on debating if this means a rate hike from the Fed is off the table. The Fed, unfortunately, can only talk about hiking or not hiking since it’s fired all its bullets and has no rate cuts to offer should the U.S. economy need a monetary boost.

What no one seems to be talking about is the serious drubbing the shares of the too-big-to-fail Wall Street banks took on Thursday and Friday of last week. That’s not something that should be swept under the rug when markets are behaving like the early days of the last financial crisis in 2008 — which saw the largest Wall Street bank bailouts in history.

While the stock losses of the largest Wall Street banks were manageable last Thursday, they picked up steam on Friday. What was particularly surprising was that JPMorgan’s losses were on a par with those of Citigroup, with Citigroup shares losing 6.06 percent in the two day period while JPMorgan was off by 6.01 percent. Bank of America, which owns the giant Wall Street stock brokerage firm, Merrill Lynch, lost 7.95 percent in the two-day span.

Citigroup is under a criminal investigation for potential money laundering in connection with its Mexican unit, Banamex, after admitting to a felony for foreign currency rigging earlier this year. One would think the investigation would cause its shares to trade at a significant deficit to JPMorgan Chase during a market rout.

Not to put too fine a point on it, but Citigroup is also the mega Wall Street bank that sucked more out of the taxpayers’ purse during the 2008 crash than any other bank in U.S. history.

Citigroup received $45 billion in equity infusions, over $300 billion in asset guarantees and more than $2.5 trillion, cumulatively, in below-market-rate loans from the Federal Reserve – all to prop up a bank that continues to this day to pay fines for malfeasance and cartel activity.

The chart above shows how Citigroup traded on Friday versus the Dow Jones Industrial Average – an index of 30 of the largest companies in the world: companies like Exxon, Coca-Cola, Boeing and Procter and Gamble.

On Friday, when the Dow closed with a loss of 531 points, Citigroup opened at $54.40 and closed at $53.60, a loss of 3.13 percent. But Citigroup made three unusual spikes during the day that were aberrational with what was going on in the broader market. We’ve noted those periods with a yellow circle on the chart above.

The most unusual move came at 2 p.m. when the Dow was deeply in red territory. Citigroup, which had opened at $54.40, traded at a high of $55.05 – levitating itself and shaking off the overwhelming negative financial news ricocheting around the globe. We’ll leave it to others to speculate on just who was buying Citigroup during those unusual spikes.

For years, Senator Elizabeth Warren and many others have been calling for real financial reform on Wall Street, including reinstatement of the Glass-Steagall Act which would separate banks holding taxpayer-backed insured deposits from Wall Street’s high-risk trading houses – putting a true end to too-big-to-fail. Tragically, we now find ourselves in the midst of a full-blown market panic with much of the financial reform of Wall Street left to the work of a future, more courageous Congress and President.

The Grecian formula emerges.

Slowly.

Without nuance.

Greece’s SYRIZA Party Splits Ahead of Snap Elections

August 24th, 2015

by Stephen Lendman

Prime Minister Alexis Tsipras was widely expected to call snap elections - Greece’s fifth general election in six years.

Twenty-nine anti-austerity SYRIZA party members bolted. They’ll challenge Tsipras despite virtually no chance to prevail. They formed a new Popular Unity party headed by former energy minister/vocal Tsipras critic Panagiotis Lafazanis.

They call it a “wide, anti-memorandum (austerity), progressive democratic front that will go to the elections with the agenda to cancel all memoranda,” a statement they issued said. They accused Tsipras of breaching his anti-austerity campaign pledge. He signed a new austerity memorandum without approval of other SYRIZA members, they explained. They continued saying: “The snap elections Alexis Tsipras decided, will be held in order to bury the proud ‘no’ of the referendum. To bury the anti-memorandum struggles and anti-memorandum expectations of the people, Greek people are asked to put a noose around their necks and approve a new memorandum.”

“The Left Platform, faithful to the SYRIZA commitments, consistent with the ‘no’ of the Greek people, carries the flag of the struggle to get out of the crisis, for productive reconstruction and progress…”

“The Left Platform will immediately form a wide, anti-memorandum, progressive democratic front that will go to the elections with the agenda to cancel all memoranda.”

“To move toward the write-off of the biggest part of the debt … To cancel austerity in wages, pensions and social spending. To stop the sellout of Greece’s state property. To put the country on a new path of national independence, sovereignty, recovery and a new progressive course.”

Lafazanis said “(a) new power is coming to the fore…(W)e will not fall victim to blackmail. We want to become a great movement that will sweep the bailouts aside.”

“The country cannot take more bailouts. We will either finish off the bailouts, or the bailouts will finish off Greece and the Greek people. The country cannot breathe and stand on its feet unless a big part of the debt is cancelled.”

Popular Unity’s stated objectives are canceling Greece’s three bailouts, writing down or renouncing its odious debt, and leaving Eurozone bondage “if necessary” to regain Greek sovereignty and help it recover and grow.

It remains to be seen how voters react to this message. With snap elections a month away, there’s precious little time to enlist enough support to matter.

Candidate Tsipras made glowing pledges. Straightaway in office he breached them. Are Popular Unity members different? Politicians of all stripes notoriously make promises they systematically compromise or violate if elected.

It’s hard imagining anything in prospect able to end Greece’s long nightmare. Its political class is beholden to Troika monied interests running things.

No party is strong enough to win majority control. SYRIZA will likely retain enough support to govern with one or more coalition partners.

Popular Unity has no chance to change bailout terms or end what Paul Craig Roberts calls Greece’s “foreign occupation.”

Western monied interests intend looting the country, pillaging its crown jewels, keeping it debt entrapped, exploiting its people more than already, destroying its sovereignty, and making it a dystopian Troika controlled colony - a testimony to predatory capitalism’s viciousness no one should tolerate.

-###-(Stephen Lendman lives in Chicago and can be reached at lendmanstephen@sbcglobal.net.

His new book as editor and contributor is titled "Flashpoint in Ukraine: How the US Drive for Hegemony Risks World War III".)

No comments:

Post a Comment