WTF!

Up against the wall.

This is the most incredibly bad news.

And so unbelievable.

I loved this man, this gifted, matchless artist.

I'll never forget how his beautifully moving music informed my youth.

What bliss it was to spend an afternoon in my dorm room listening to the Airplane, and then the Starship, and then all of the other transmutations of musical envelopmentness that he and they provided.

That's how it felt: completely enveloped in blissful love.

I had all his/their albums.

What a happy life.

I was kissed by Jorma and Jack one afternoon before a performance.

What phenomenal luck.

But never Paul.

I was never close enough.

But he was an idyll provider for me.

Paul Kantner can not pass away.

Sail on, sailor.

You sailed into our hearts.

To stay.

5 Wall Street Banks Have Lost $219.7 Billion in Market Cap in 7 Months

We get the inside word on how the Obama exit from the national stage will be managed from the "New York Times:"

BALTIMORE — When President Obama addressed the annual retreat for House Democratic lawmakers in 2009, the event had the buoyant exuberance of a pep rally as he urged his party’s robust majority — then 257 members strong — to help muscle through his economic stimulus plan.

But as Mr. Obama speaks at this year’s retreat here on Thursday evening, he will stand before a far smaller and less popular audience: 188 Democratic lawmakers in a minority caucus with virtually no chance of moving back into power in the November elections.

. . . Some Democrats hold Mr. Obama responsible for that, saying their party’s lawmakers took the blame for the president’s aggressive and often unpopular agenda to revive the economy and adopt sweeping health care legislation during his first two years in office. And some say Mr. Obama showed indifference to the political circumstances of rank-and-file lawmakers and missed an opportunity to seize on the undercurrents of populism and anti-establishment sentiment that began coursing through the electorate after the partisan battle over health care.

“The main Democrat nationally, and the only one who could be heard, was silent on the huge structural issues that more and more Americans were facing,” said Stanley Greenberg, a veteran Democratic pollster who blames Mr. Obama for Democratic House losses in 2010 and 2014. “His silence on those things left the voters without much motivation to vote.”

Mr. Greenberg said Mr. Obama and Ms. Pelosi would be remembered for making transformative changes during 2009 and 2010, when the president confronted an economic crisis, Ms. Pelosi wielded the speaker’s gavel to corral support, and Senate Democrats controlled the 60 votes needed to overcome Republican filibusters.

“We will look at those two years as enduring,” he said. But he said Mr. Obama’s legacy would also include the political death of Ms. Pelosi’s once-powerful majority. “Part of his legacy is the off-year elections,” he said.

Administration officials reject that critique, noting the historic pattern of losses that a president’s party often sustains in off-year elections and the eight House seats Democrats regained when Mr. Obama was on the ballot in 2012. They say Mr. Obama was a prolific fund-raiser and a frequent campaigner for Democratic candidates whenever he was asked; the president hosted 17 fund-raising events across the country in 2013 and 2014, they said.

Some Congressional Democrats said it was not enough — not necessarily because Mr. Obama could have done more but because there could never be enough fund-raising given the nature of modern political campaigns. “If the president had allocated 50 more of his days to raising money,” Representative Brad Sherman, Democrat of California, said at a reception to mark the start of the retreat in Baltimore, “we would have more Democratic members here.”

In a lunchtime speech here, Vice President Joseph R. Biden Jr. told the Democratic lawmakers he believed that they could win back the House if they drew a sharper contrast with Republicans.

“I think we can win; I think the House we can win,” Mr. Biden said. “I think we have to focus — and we didn’t do it enough the last time in my view. The best way to win is to run on what we have done and what we stand for, and run on what more we are trying to do, making clear what we think we have to do to finish the agenda and then contrast that to what they are for and what they oppose.”

As for Republicans, he said, “They opposed every single, solitary initiative that you supported over the last seven years if you were here that long to support this recovery.”

And, yet, not a word about the massive state gerrymandering that has eliminated representative districts by drawing districts that put the vast majority of Democratic voters in a few closely-packed districts versus the more numerous sparcely-populated Republican-dominated districts.

Let alone all the (frigging new) wars and drone victims that have occurred in the last seven years.

I'm sure these had nothing to do with the Democratic voters who didn't vote (or voted for another party).

The "New York Times!"

Stand up and take a bow.

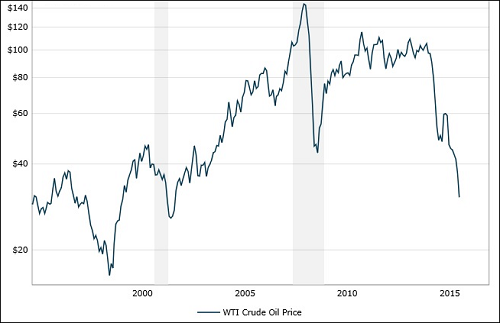

Those hearings triggered an in-depth investigation and more outrageous disclosures in 2014 of an out-of-control Wall Street by the Senate’s Permanent Subcommittee on Investigations, then chaired by Senator Carl Levin, another Senator that refused to be silenced by Wall Street. Levin’s Subcommittee found that Wall Street banks had set up secret shell companies to gain control of a stunning amount of the nation’s industrial commodities – such as oil, aluminum, copper, natural gas, and even uranium – on a scale that “appears to be unprecedented in U.S. history,” according to a 400-page report released by the Subcommittee.

Since Republicans took control of both the Senate and House in January 2015 and appointed their own Committee and Subcommittee chairs, we’ve heard almost nothing further about this critical matter – proving once again how Wall Street gets its way on Capitol Hill.

Not that I agree that Obama is worried about how his legacy will be viewed, but the rest of the essay below is pretty much spot on.

Go Bernie!

Bernie Sanders Meets With Obama Today: What They Might Talk About

By Pam Martens and Russ Martens

January 27, 2016

Expensive media real estate is reporting that presidential candidate, Senator Bernie Sanders of Vermont, will meet with President Obama in the Oval Office today. Much is being made of the fact that the meeting comes less than a week before the politically important Iowa caucuses and just two days after "Politico" published an exclusive interview with the President in which he appeared to favor a Clinton presidency. (Memo to the President: this election is about finding an authentic non-establishment candidate, so your opinion as the quintessential establishment figure is not likely to sway folks – at least not in a good way.)That’s the essence of restoring the Glass-Steagall Act and curtailing the unbridled looting of the public by the Wall Street machine.

The first thing that came to mind when we heard about the meeting was that one or more kingpins on Wall Street might have asked the President to whisper in Senator Sanders’ ear to stop repeating at every campaign stop that the business model of Wall Street is fraud. Sanders is also regularly stating on the stump that one of his top priorities as President will be to break up those Wall Street banks that would require another taxpayer bailout if they should fail.

Would Wall Street actually be brazen enough to try to censor the message of a sitting U.S. Senator? Back in March of last year, Reuters reported that representatives of Citigroup, JPMorgan, Goldman Sachs and Bank of America “have met to discuss ways to urge Democrats, including [Elizabeth] Warren and Ohio Senator Sherrod Brown, to soften their party’s tone toward Wall Street.” The article noted that withholding campaign donations to Senate Democrats was one option that was on the table at the Wall Street banks.

Wall Street’s guns were out for Senators Elizabeth Warren and Sherrod Brown because both were mincing few words about the serial corruption on Wall Street. Senator Warren is also a lead sponsor of legislation to separate insured deposit banks from investment banks and brokerage firms that speculate in stocks, bonds and derivatives, thus restoring the Glass-Steagall Act that successfully protected the country’s financial system for 66 years until the Bill Clinton administration repealed it in 1999. Just nine years after its repeal, Wall Street imploded in a fashion similar to the 1929 crash – the reason that the Glass-Steagall Act was enacted in the first place in 1933.

Senator Sherrod Brown had raised eyebrows on Wall Street with his hearings that rooted out the unfathomable levels of physical holdings of oil, metals and other commodities that a negligent Federal Reserve had allowed Wall Street banks to take ownership of and control, unilaterally repealing decades of banking law with no Congressional input or even awareness.

Those hearings triggered an in-depth investigation and more outrageous disclosures in 2014 of an out-of-control Wall Street by the Senate’s Permanent Subcommittee on Investigations, then chaired by Senator Carl Levin, another Senator that refused to be silenced by Wall Street. Levin’s Subcommittee found that Wall Street banks had set up secret shell companies to gain control of a stunning amount of the nation’s industrial commodities – such as oil, aluminum, copper, natural gas, and even uranium – on a scale that “appears to be unprecedented in U.S. history,” according to a 400-page report released by the Subcommittee.

Since Republicans took control of both the Senate and House in January 2015 and appointed their own Committee and Subcommittee chairs, we’ve heard almost nothing further about this critical matter – proving once again how Wall Street gets its way on Capitol Hill.

Say something nice, if you say anything at all, about Wall Street became the mantra back in 2013. CNBC’s Maria Bartiromo (now on Fox) appeared on NBC’s "Meet the Press" on September 15, 2013 – the fifth anniversary of the Wall Street crash. Bartiromo had this to say:

Bartiromo: “We need to get beyond the conversation of is Wall Street evil, are the bankers evil and causing pain; and toward the conversation of, how do you create sustainable economic growth? That will answer the issue of inequality. Because with growth comes jobs.”Fortunately for Americans, there are still Democrats in the U.S. Senate and a handful of Republicans who understand that Wall Street’s serial corruption and wealth transfer system is at the very heart of wealth and income inequality in America. America is also fortunate to have one Presidential candidate, Senator Bernie Sanders, who is serious about changing this reality.

Just last week we were reminded of just how little progress has been made on reforming Wall Street since President Obama took office in January 2009. JPMorgan Chase said in filings that it had awarded its Chairman and CEO, Jamie Dimon, total compensation of $27 million for 2015, an increase of 35 percent from the prior year. The obscene compensation came despite the fact that Dimon’s company became an admitted felon in 2015 for rigging foreign currency (Forex) markets. No major U.S. bank had ever before carried the taint of felon in U.S. financial history. After an unprecedented run of serial crimes against the investing public, detailed here by two attorneys who think this is on a par with a crime syndicate family, why is Jamie Dimon even still heading a major Wall Street bank, let alone getting a 35 percent pay increase?

The two attorneys, Helen Davis Chaitman and Lance Gotthoffer, who published a book about JPMorgan’s facilitation of the Bernie Madoff Ponzi scheme (which garnered it a deferred prosecution agreement from Eric Holder’s U.S. Justice Department), wrote the following about Dimon and JPMorgan Chase in May of last year:

“If Carlo Gambino were alive, he’d be kissing the toes of Jamie Dimon out of abject admiration. Gambino and his cronies were like small-time pickpockets by comparison; and they went to prison for their crimes. They could never have foreseen that America would be run by the Obama/Holder team. As we demonstrated in Chapter 4 of JP Madoff, it is no exaggeration to say that JPMorgan operates like a crime syndicate. That’s why we suggested in Chapter 5 that it be criminally prosecuted under RICO — and punished like the members of other crime syndicates have been punished. And, believe it or not, even the participants in the Forex scheme knew they were acting like organized crime does.On the same day last week that the news broke of Dimon’s obscene pay, the "Dow Jones" news site, "MarketWatch," published an article revealing that Wall Street is underwriting a significant amount of Initial Public Offerings (IPOs, meaning companies being sold to investors as publicly traded companies for the first time) whose auditors have issued a “going concern” warning. This warning, as the article explains, means that auditors are signaling that “there is reasonable doubt the company can stick it out over the next year — also frequently leads to a bankruptcy filing.”

“In its plea agreement with JP Morgan, the DOJ recites it had evidence sufficient to prove that: ‘In furtherance of the conspiracy, the defendant [JPMorgan] and its co-conspirators engaged in communications, including near daily conversations, some of which were in code, in an exclusive electronic chat room which chat room participants, as well as others in the [relevant] Market referred to as ‘The Cartel’ or ‘The Mafia.’ ”

The job of Wall Street is to fairly and responsibly allocate capital to companies which can help America grow and create good-paying jobs.

Underwriting IPOs for companies whose time frame for surviving may be less than a year sounds like a replay of the Dot.com Bust of 2000 which destroyed trust in Wall Street and wiped out $4 trillion of investors’ wealth.

A third article came out last Thursday from Mark Karlin, Editor of "Buzzflash" at "Truthout," calling attention to Senator Warren’s upbraiding of Obama’s Justice Department’s and other regulators’ settlement with Goldman Sachs over its subprime mortgage abuses. Senator Warren had this to say on her Facebook page:

“In the 2008 financial crisis, we lost trillions in wealth and millions of people lost their homes and their jobs because of Wall Street recklessness. Today, Goldman Sachs announced it will pay $5.1 billion for its role in precipitating the economic collapse by misleading investors about the quality of the junk mortgage securities they peddled. Seven years later. No admission of guilt. No individuals are going to jail. A payment that’s barely a fraction of the billions investors lost – and the trillions our economy lost – because of this fraud. And over half of it could be tax deductible! That’s not justice — it’s a white flag of surrender.”President Obama is clearly worried about his legacy and his career prospects that will ensue from that legacy. The time to have worried about that was when he contemplated who should run his Justice Department and his Treasury Department and his SEC. Thanks to those decisions, the country has a great deal more to worry about now than the President’s legacy.

All it would take to set America back on the right financial course are these 31 words in Wall Street reform legislation:

“No bank holding insured deposits can own or be affiliated with an investment bank, broker-dealer, futures commission merchant, insurance company or engage in the underwriting of stocks, bonds or derivatives.”

And when it goes down again . . .

It goes downnnnnnn.

Hello 4th world!

No comments:

Post a Comment