Stop Blocking Voting Rights Bills, Activists Tell House Judiciary Chair

Meet The New Police Reform Bosses

The Saudis Have Been “Punching Above Their Weight Class,” Militarily and Economically

With everything happening right now in the world ~

I just can't stop checking in with the Martens every day for my personal economic demise rate.

Can you?

Big Bank Moral Hazard: A Look at Paul Volcker’s Fed and June 30, 1982

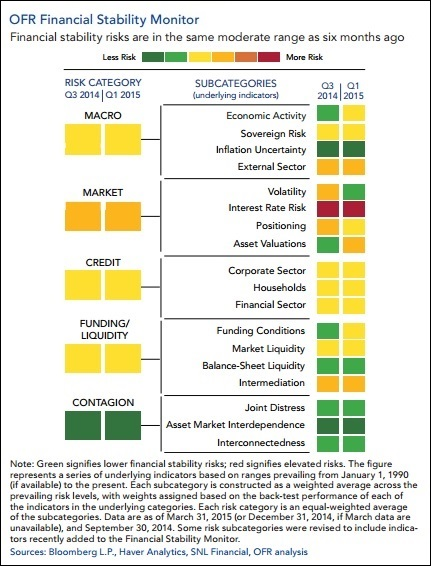

Treasury Now Has Color-Coded Financial Terror Alerts

By Pam Martens and Russ Martens

June 25, 2015

Remember when the Department of Homeland Security was issuing those color-coded terrorist alerts? Well, they don’t do that anymore. They’re back to using plain ole black-and-white words to describe threats.

Apparently, however, the U.S. Treasury’s Office of Financial Research (OFR) thought it was such a cool idea that they’ve started color-coding threats to our financial security from the denizens on Wall Street: the gang that brought our country to its knees in 2008 while the most expensive military in the world was hunting down robed cave-dwellers in the Middle East.

Sorry about my loss of computer with which to post my economic comments, articles, essays and collaborative efforts.

When it gets over 10 years old, something starts to happen.

And it's not good.

(Send money if you want quicker service.)

Here's a recent (but not this week's) post on what's really happened to Greece.

And why we should all be very worried about what the banksters-in-charge have in store for US.

Read it and weep.

Germany could turn out to be going soft on them. (It's a tough read, friends, but it won't take a whole beer.)

3 June 2015

Greece: Out of Cash, Out of Time, Out of Options

On Friday Greece is due to pay at least a quarter of the €1.5bn due to the IMF in June. It appears that, if it has the money to cover that bill at all, it thinks it needs to hold on to it to pay internal Greek payments (public sector salaries etc). It says it will only pay if there is an agreement with its Eurozone, IMF and ECB creditors to disburse the final €7.2bn from the previous Greek bailouts that has been argued about since February.

- Greece: out of cash, out of time, out of options

- The Eurozone does not want to make any compromise with the current Greek government

- Syriza believes default or Grexit would be better than continuing with austerity now

The creditors say they will only disburse the money if the Greek government enacts various key economic reforms and does not roll back reforms the last government agreed with the lenders and if the Greek government undertakes to run large enough budget surpluses every year in the future that Greece might have a chance of paying back the money the creditors have lent it. The Greek government says there is no possibility of it ever paying back all the money it has been lent and the creditors need to accept that, write off some of the debt, and not insist that Greece runs large surpluses (predicated on the fantasy of paying back the debt) or cuts back on pensions or enacts other similar measures that run contrary to the Greek voters’ will (as expressed in the last election).

Most commentary still appears predicated on the idea that there will be some last-minute deal — either because the creditors will back down and give Greece some more money without requiring it to be paid back or because the Greek government will back down if it understands that not doing so would ultimately mean leaving the euro.

I, on the other hand, don’t believe either side is particularly interested in achieving a deal. The Eurozone does not want to make any compromise with the current Greek government because (a) they don’t believe they need to because Greek threats to leave the euro are empty both because internal polling suggests Greeks don’t want to leave and because if they did leave that doesn’t really constitute any threat to the euro; (b) because they (particularly perhaps Angela Merkel) believe that under enough pressure the Greek government might collapse and be replaced by a more cooperative government, as has happened repeatedly before in the Eurozone crisis including in Italy and Greece itself; and (c) because any deal with Greece that is seen to involve or be presentable as any victory for the Greek government would threaten the political positions of governments in several Eurozone states including Spain, Portugal, Italy, Finland and perhaps even the Netherlands and Germany.

Furthermore, it’s not clear to me that the Eurozone creditors at this stage would have much interest in any deal based upon promises, regardless of how much the Greek had verbally surrendered. Things have gone too far now for mere words to work. They would need to see the Greeks deliver actions — tangible economic reforms and tangible, credible primary surplus targets and a sustainable change in the long-term political mood within Greece that meant other Eurozone states might eventually get their money back. That is almost certainly not doable at all with the current Greek government. The only deal possible would be with some replacement Greek government that had come in precisely on the basis that it did want to do a deal and did want to pay the creditors back.

On the Syriza side, I see no more appetite for a deal. They believe that austerity has been ruinous for the lives of Greeks and that decades more austerity would mean decades more Greek economic misery. From their point of view, default or even exit from the euro, even if economically painful in the short term, would be better than continuing with austerity now. The only kind of deal they could countenance would be one in which creditors accepted that austerity must end and much of the monies lent are never coming back.

Even though neither side thinks a deal is possible with the other, they keep talking and keep telling the world a deal is close because (a) some on the Eurozone side continue to hope that under enough pressure the Greek government might collapse or make some bad political mistake that leads to its downfall; (b) the Eurozone does not want to eject the Greeks – it wants them to choose to leave, instead, if indeed they do leave in the end; (c) the Greek government wants to be thrown out or, if it chooses to leave in the end, to be able to say credibly to the Greek people (who continue to be in favour of euro membership — though that is no longer true of the majority of Syriza voters, 58 per cent of whom now say in opinion polls that euro exit would be preferable to more austerity) that it tried everything and euro exit was a final resort.

The past 24 hours have seen an alleged “Take-it-or-leave-it” proposal from the Eurozone, which reports indicate appears to involve no debt relief at all, no material change in the demands for economic reforms, and primary surpluses of 1% in 2015, 2% in 2016, 3% in 2017, and 3.5% thereafter. Since the Greek economy has deteriorated further through 2015 with the political turmoil, a 1% target might be difficult to meet and at this stage is no kind of “compromise”, whilst the 3.5% longer-term target continues to reflect the narrative of placing the Greeks in a position to repay their debts, which the Greek government refuses to accept. It is hard to see how Syriza could accept that without collapsing. If it really is “take-it-or-leave-it” then if Syriza wants to contemplate it at all that might mean a referendum – which would presumably lead to a rejection. I suspect they will simply start the defaulting on Friday by not paying the IMF.

On the other side, the Greek made their own counter-proposals. The German finance minister Wolfgang Schaeuble — who publicly said some time ago that no-one had any idea how a deal could be reached — said public statements of optimism were not justified and that his impression of the Greek proposals was that talk won’t be over soon.

And yet, even if all the current excitement about an imminent deal, within hours or a few days, were justified, what would it really mean? They are still only debating the conditions for the disbursement of the final €7.2bn from the previous Greek bailouts! Even if they agree to that, which would cover the €6.5bn or so that Greece needs to get through June, that would still leave Greece with no way to pay its large debts to the ECB and others that are due in July and August. To get through the summer, there would need to be another whole bailout agreement, covering around €30-50bn more given to Greece and including a whole additional set of economic reforms and surplus targets! Which Eurozone Parliament is going to vote for that?

The Economic Collapse Blog Has Issued A RED ALERT For The Last Six Months Of 2015

No comments:

Post a Comment