Jebbie's Campaign Platform Is More Punishment for Those at the Bottom (Workers Just Need to Work More Hours to Get Ahead He Whines)

Dubya (Still Alive and Kicking) Thinks Being Paid a Million Dollars Plus Expenses to Speak to Wounded Iraq and Afghanistan Soldiers Is Insufficient Remuneration for his War Service to Grateful Country

U.S. Has Contrived Orwellian Opposition To What Real Leadership Should Create: Literal Criminal Fraud

Stay At Home Voters Know That There Is NO ONE To Vote For (Except Alan Grayson)

I'm not normally a suspicious person. Or a naive one. But when I see obvious looting going on by the wealthy (in this case, the very wealthy who don't "need" the money (one would think)), who are gleefully taking all they can as quickly as they can from the rest of the world's population, the words that come to mind are "Business as usual."

And "usual" just got cranked up. Greece has been told by their creditors that Sunday is its last day before financial oblivion (so to speak).

Or before Grexit.

Please try to view Chris Hedges' "Days of Revolt" on Link TV this week to shop for more steel (if you're in the market for it) for your spine (and it's on right now). It seems that the steel sale is going great guns (so to speak) internationally now. Any of Hedges' programs on Link TV or Free Speech TV (FSTV) will be edifying in addressing the task of stopping the looting. Also, don't miss "Democracy Now" for the only meaningful reporting on what's happening in Greece (and the European Union/Germany/etc.) with Drs. Richard Wolfe, Paul Mason and many other knowledgeable commentators.

As to what's happening right now?

Here are a few essays to study closely as we await the next events reported on "Democracy Now" (and yes, you'll need more than one drink to take in everything here):

Where Greece Should Go from Here

ECB Is Trying to Break Greece: Buckle or Leave the Euro

July 7, 2015

Greece And The EU Situation

Paul Craig Roberts

I doubt that there will be a Greek exit.

The Greek referendum, in which the Greek government’s position easily prevailed, tells the troika (EU Commission, European Central Bank, IMF, with of course Washington as the puppet master) that the Greek people support their government’s position that the years of austerity to which Greece has been subjected has seriously worsened the debt problem. The Greek government has been trying to turn the austerity approach into reforms that would lessen the debt burden via a rise in employment, GDP, and tax revenues.

The first response of most EU politicians to the Greek referendum outcome was to bluster about Greece exiting Europe. Washington is not prepared for this to happen and has told its vassals to give the Greeks a deal that they can accept that will keep them within the EU.

Washington has a higher interest than the interests of the US financial interests who purchased discounted sovereign debt with a view toward profiting from a deal that pays 100 cents on the dollar. Washington also has higher interest than the interests of the European One Percent intent on using Greece’s indebtedness to loot the country of its national assets. Washington’s higher interest is the protection of the unity of the EU and, thereby, NATO, Washington’s mechanism for bringing conflict to Russia.

If the inflexible Germans were to have Greece booted from the EU, Greece’s turn to Russia and financial rescue would put the same idea in the heads of Italy and Spain and perhaps ultimately France. NATO would unravel as Southern Europe became members of Russia’s Eurasian trade bloc, and American power would unravel with NATO.

This is simply unacceptable to Washington.

If reports are correct, Victoria Nuland has already paid a visit to the Greek prime minister and explained to him that he is neither to leave the EU or cozy up to the Russians or there will be consequences, polite language for overthrow or assassination. Indeed, the Greek prime minister probably knows this without need of a visit.

I conclude that the “Greek debt crisis” is now contained. The IMF has already adopted the Greek government’s position with the release of the IMF report that it was a mistake from the beginning to impose austerity on Greece. Pressured by this report and by Washington, the EU Commission and European Central Bank will now work with the Greek government to come up with a plan acceptable to Greece.

This means that Italy, Spain, and Portugal can also expect more lenient treatment.

The losers are the looters who intended to use austerity measures to force these countries to transfer national assets into private hands. I am not implying that they are completely deterred, only that the extent of the plunder has been reduced.

As I have previously written, the Greek “debt crisis” was an orchestration from the beginning. The European Central Bank is printing 60 billion euros per month, and at any time during the “crisis” the ECB could have guaranteed the solvency of any remaining creditor banks by purchasing their holdings of Greek debt, just as the Federal Reserve purchased the troubled mortgage backed “securities” held by the “banks too big to fail.”

This easy solution was not taken.

The orchestration was a benefit to Western financial interests in general by enabling enormous speculations on the euro and gambling with derivative bets on sovereign debt and everything connected to it. Each successive “crisis,” such as Sunday’s "No" vote, became cover for an attack on oil or other commodities. The rigging and manipulation of markets can be hidden by pointing fingers at the latest “crisis.”

John Perkins in his book, Confessions of an Economic Hit Man, describes the process by which Western financial interests intentionally over-lend to weaker countries and then use the pressure of the debt to force the transfer of the countries’ wealth, and often sovereignty, to the West. The IMF and its austerity programs have long played a role in the looting.

In exchange for reducing euro debt on Greece’s books, Greece was to turn over to private interests its water companies, ports, and protected islands. Unless the One Percent can purchase the current Greek government as it purchased previous governments (for example, with payoffs to borrow money with which to purchase submarines), the referendum has frustrated the looters.

In my book, The Failure of Laissez Faire Capitalism, I explained that the Greek “debt crisis” had two other purposes. One was to get rid of the practice of restructuring a country’s debt by writing it down to a level the country could afford and to establish in its place the new principle that people of a country are responsible for the mistakes of creditors who over-lend. The write-down is no longer to occur on the balance sheet of the creditors’ but instead becomes a write-down of pensions, social services, and employment. This, too, is a process of looting.

The other purpose, as Jean-Claude Trichet, the previous head of the European Central Bank, made explicitly clear, was to further reduce the sovereignty of member states of the EU by transferring authority over fiscal policy (tax and spend decisions) from national governments to the EU in Brussels.

Washington favors this centralization of political power in Europe, and Washington favors the One Percent over the people. However, above all Washington favors its own power and has acted to prevent a Greek exit, which could begin the unraveling of NATO.

Russia and China have missed an opportunity to begin the unraveling of NATO by assisting Greece’s departure from the EU. Whatever the cost, it would be tiny in comparison to the military buildup that Washington is forcing on both countries. Russia and China might have decided that Washington could no more accept Greece’s alignment with Russia than Russia can accept Ukraine becoming a member of NATO.

If the Greek situation and the waiting Italian and Spanish situations are now resolved along the lines that this article suggests, it means that the NATO mechanism for Washington’s pressure on Russia remains intact and that the conflict that Washington has created will continue. This is the bad news and the downside of Greece’s victory over the looters.

(Dr. Paul Craig Roberts was Assistant Secretary of the Treasury for Economic Policy and associate editor of the "Wall Street Journal." He was columnist for "Business Week," "Scripps Howard News Service," and "Creators Syndicate." He has had many university appointments. His internet columns have attracted a worldwide following. Roberts' latest books are The Failure of Laissez Faire Capitalism and Economic Dissolution of the West and How America Was Lost.)

Athens Agonistes: Troika Extremists Write New Greek Tragedy

Chris Floyd

29 June 2015

The people of Greece are being driven to their knees by a gang of brutal religious extremists, willing to destroy whole nations for the sake of something that doesn't even exist. Yet the 'civilized' world cheers these barbarians on as they despoil the cradle of Western democracy.

Greece is facing total collapse unless it knuckles under to the draconian demands of the bizarre cultists known as the Troika, a sinister union of three extremist groups (the I.M.F., the European Central Bank and the European Commission) who seek to impose their harsh and rigid way of life across the world. They insist that control of a nation's wealth be given over to a few powerful emirs and the Troika's favored moneylenders in its richer satrapies.

All measures designed to aid the common good and build a decent life for ordinary citizens are ruthlessly suppressed by the Troikaists. Public resources are forcibly sold off - at knock-down prices - to foreign interests or local lordlings. The fact that millions of people are left destitute, living diminished lives in crumbling infrastructure, growing sicker, weaker, more hopeless, even dying from want and neglect - none of this matters to the ruthless fanatics. All that matters is obedience to their will, and adherence to the Troika's bleak and joyless system for the regulation of life, which its learned theologians call "austerity."

The supremely comfortable, self-satisfied burghers and bankers who control the Troika's factions, along with their dutiful servants in government, are watching, impassively, as the Greeks twist and turn in the poisonous shirt of Nessus that the cult has forced upon them. Already brought low by years of austerity adopted by their leaders in a vain attempt to placate the Troikaist hordes at the border, this week the Greek people face the final reckoning: complete submission, which guarantees more ruin, or a terrifying leap into the unknown, refusing the demands and suffering whatever acts of revenge the Troika will wreak upon such heretics.

It's a remarkable situation. Millions of human beings are suffering, and for what? To repay a few powerful financial institutions for the loans they gave to the Greek government - loans which, by odd coincidence, were actually spent almost entirely on servicing previous debt to those same financial institutions. Very little of it went into the Greek economy, as the "NY Times" notes.

It was a case of taking on new debt to pay off old debt (a situation not unknown to many of us, I'm sure), as the country slipped further into decay.

Yet it was not enough for the cultists to loan money for Greece to give right back to them; they also required that Greece restructure its society, government and economy to fit the Troika's neoliberal straitjacket. Taxes had to be raised. (For ordinary folk, of course; rich Greeks - like the rich everywhere - can still use complex tax-dodging schemes to stash their cash offshore.) Government spending - especially on such useless trash as pensions, welfare, education, healthcare - had to be ruthlessly slashed. The labor market had to become more "flexible" - that is, stripped of job protections and workers rights, making it easier to fire people or pay them less. Deregulation and privatization were also commanded.

But why? The ostensible reason was that these austerity measures would make the Greek economy roar like a lion in his prime. But even an economist is smart enough to see that making a bankrupt country even poorer and more desperate while preventing it from injecting bailout funds into its economy is a recipe for ruination, not a blueprint for growth. And the past four years have proved that Troika’s austerity sharia has not and cannot produce “growth” in a broken economy with 25 percent unemployment. (The same percentage as in the US during the depths of the Great Depression.)

And why this time limit on the repayment? Even on the relatively small down payment (around $1.5 billion) being demanded immediately - a payment that the bankrupt nation simply can't pay at the moment. Why not stretch the payments out - way, way out, if necessary? After all, Britain only paid off its post-World War II rebuilding loan from the United States in 2006 - exactly 50 years after it was given. Why couldn't Greece be given the time to work out its economic problems - in its own way, without mutilating its society - and pay back its debts over the long haul?

But of course it’s not about the money. As many have already pointed out, the Troika knows that Greece is bankrupt and can’t pay back the money. (Unless, as with the UK, they are given generations to do so, on easy terms that don’t require them to bleed their people dry and gut their own society.) No, the current squeeze on Greece is about the system, the imposition of "austerity sharia" that is the lodestar of the Troika’s blinkered religious beliefs. If Greece will not accept the system, then it must be punished, it must be made an example. In short, it’s an act of terroristic PR, like the ISIS beheading videos: a warning that this is the fate of all those who refuse to submit.

What, in the end, is at stake? Literally nothing. Numbers on a computer screen. It’s not as if Greece has a hoard of German gold hidden in the Acropolis and won’t give it back. It’s not even as if the Greeks have warehouses full of banknotes that they can send back to the Troika. All of it — the debts, the loans — are abstract notions. The debt could be written off with the press of a delete key, or reduced by the subtraction of a zero or two on a digital spreadsheet.

So could the losses of the lenders. (Although why shouldn’t the lenders lose their money? You put up your money, you take a risk, and if the venture fails, you lose. Isn’t that the ‘free market’ way? But of course there is no free market; there are only systems of exchange that powerful entities seek to control and manipulate to their advantage. There is no free market in any system where some enterprises are ‘too big to fail’ and must be bailed out by the sustenance of ordinary citizens.)

Money is a myth, sustained by the faith of those who accept whatever is the arbitrary measurement of value in any given time or society. (Beads, shells, axes, coins, ingots, strips of paper, liquid crystals dancing on a screen.) Yet throughout history, these myths have led to the deaths and despoliation of millions of innocent people. It is a myth that perpetuates inequality, servitude, suffering, and the dominion of a powerful few. The latest installment of this ancient tragedy is being played out right now in Greece, where tragedy was born. And the extremism being displayed by the Troika is just as mindless, destructive and merciless as that of the violent Islamists that the ‘defenders of Western civilization’ have done so much to foment in their global power games.

The Study that Foreshadowed the Three Fraud Epidemics that Drove the Crisis

February 15, 2015

William Black

I will be writing a series of articles concerning the three mortgage fraud epidemics that hyper-inflated the bubble and drove the financial crisis prompted by four recent economic studies of mortgage fraud. My goal is to integrate the results of those studies with the work of criminologists, investigators, and data from other sources such as Clayton.Second, the result was the sale of piggy-back loans that suffered significantly greater defaults and losses. I explained in my earlier column:

In economics and white-collar criminology, we teach our students the very useful concept of “revealed preferences.” We take what potential perpetrators say they would do and why they claim they took an action with cartons of salt. Their actions generally speak far louder and more candidly than do their words. I will show in this series how valuable revealed preferences are in analyzing the data and testing rival research hypotheses. (I will explain why I feel the recurrent failure to state these hypotheses expressly leads to serious error.)

I have come to the view that a concept that I term “revealed biases” is a useful corollary to “revealed preferences.” The National Institute of Justice virtually never funds empirical studies of elite white-collar criminals (a classic “revealed bias”). OMB suggests research programs exclusively for blue collar crime – in the midst of the largest and most destructive epidemics of elite white-collar crime in history. I wrote my first column in this series about an example of revealed biases in discussions of econometric studies of mortgage fraud.

The Piskorski, Seru, and Witkin (PSW) Study

The four studies can be read without charge. (The most recent study was behind a pay wall when I wrote by first article in this series.) In this and my next column I discuss two excellent studies by multiple authors. I have written previously about a February 2013 study entitled: “Asset Quality Misrepresentation by Financial Intermediaries: Evidence from RMBS Market.” The co-authors are Tomasz Piskorski (Columbia GSB), Amit Seru (University of Chicago and NBER), and James Witkin (collectively, PSW). (RMBS is an acronym for Residential Mortgage-Backed Securities.) (I discussed the PSW study extensively in an academic talk I gave on February 26, 2013 at Columbia that Piskorksi was able to attend.)

This column begins the process of showing how adding the research findings and theoretical developments of criminologists, (effective) regulators, and economists on “control fraud” (aka “looting”) to the excellent work by of these finance authors can be useful to understanding the ongoing crisis and limiting or even preventing future crises. This column focuses on the PSW study’s findings and a few key interpretations of those findings.

The next column discusses the most recent study on liar’s loans by Amir Sufi and Atif Mian.

The PSW study looked at two forms of mortgage fraud – misrepresentation as to the borrower’s intent to occupy the home as his primary dwelling and the absence of a “piggy-back” loan (in which the borrower pays the down payment on the first lien loan partially or completely from the proceeds of the “second” (contemporaneous) lien loan). Both forms of misrepresentation increase the probability of default and the likely loss upon default. There were four key findings from the PSW data. First, our most elite banks defrauded secondary market purchasers by falsely claiming that the loans were not piggy-backs.

“[A]lthough there is substantial heterogeneity across underwriters, a significant degree of misrepresentation exists across all underwriters, which includes the most reputable financial institutions” (PSW 2013: 29).

“The PSW 2013 study documents that the officers controlling the home lenders knew the representations they made to the purchasers as to the lack of a second lien were often false (pp. 2, 5 n. 6), that such deceit was common (p. 3), that the deceit harmed the purchasers by causing them to suffer much higher default rates on loans with undisclosed second liens (pp. 20-21), and that each of the financial institutions they studied – the Nation’s “most reputable” – committed substantial amounts of this form of fraud (Figure 4, p. 59).”Third, the banks often misrepresented (frequently unintentionally) to secondary market purchasers whether the borrower would occupy the home as his principal dwelling. The study infers from the pricing that the lenders were often dubious of the speculators’ representations about their intent to occupy and partially compensated for this risk by charging them a higher interest rate despite their representation to the lender that they intended to occupy the home

Fourth, the data suggest that, as a group, the borrowers who misrepresented their intent to occupy were more likely to default, but that the borrowers in the cases where the piggy-back loans were misrepresented were not materially more likely to default than borrowers with (disclosed) piggy-back loans. The contrast can be seen in Figure 2 (p. 56), Panels A & B. Panel A shows that the default rate for misrepresented non-occupants is much higher than the default rate for those who disclose that they plan to be non-occupants.

This is consistent with severe adverse selection when lending to borrowers who misrepresent their intent to occupy. By contrast, Panel B shows that default rates are very similar between borrowers in which there is a piggy-back loan regardless of whether the piggy-back loan was disclosed. Loans that were not piggy-back loans (i.e., loans with a real down payment) had a substantially lower default rate than loans with a piggy-back regardless of whether the piggy-back was disclosed on the loan application. This suggests that there is no material adverse selection in this context arising from differences in the borrowers’ integrity. It also suggests that it was the lenders’ officers’ idea to misrepresent the existence of the piggy-back second lien.

These two forms of mortgage fraud were very large – except compared to the two great epidemics of mortgage origination fraud (liar’s loans and inflated appraisals) and the resultant secondary market frauds when these fraudulently originated mortgages could only be originated through fraudulent “reps and warranties.” The piggy-back fraud was obviously generated by the lenders because they had made both the first and second lien loans contemporaneously, but the(y) made reps and warranties that they were not piggy-back loans. The lenders obviously did not rely on any representation from the borrowers that the contemporaneous piggy-back loans that the banks were making to the borrowers were not piggy-back loans.

The situation with misrepresentations about the borrower’s intent to occupy the home as his principal dwelling is more complex. The borrowers made the misrepresentations and they are investors or “speculators” who buy multiple homes either to rent them or “flip” them. It is difficult for a lender to check on the validity of the “intent to occupy” representation, but verifying the borrower’s assets and checking his tax returns will disclose any substantial speculators. The complexity in interpreting the results is that while the lending officials would prefer to make the loan with the risk premium added for non-occupancy, many of them would prefer to make the loan without that risk premium if the alternative was losing the loan to a rival lender that did not charge such a premium.

It is certain that some lenders signaled their willingness not to check on the accuracy of occupancy representations by borrowers. It is also very likely that some lenders reached an intermediate position of not checking vigorously on occupancy representations and not charging the full non-occupancy risk premium, but charging an intermediate rate with a moderately higher risk premium while pulling a “wink, wink; nod, not” when it came to loan approvals to borrowers the lenders believed to be likely speculators. Econometric studies cannot answer these questions, though detecting a partial risk premium is helpful in drawing inferences.

The critical takeaway from the PSW study is that the most elite lenders and RMBS underwriters were shown to have knowingly and intentionally have engaged in fraud in a significant number of piggy-back loans. Those loans were far more likely to cause severe defaults and more severe loss upon default because the loan-to-value (LTV) ratio was so extreme. The loan servicer was certain to discover that there were two, simultaneous liens when the loans defaulted.

The lender that made the rep and warranty that there was no second lien was the lender that made both loans, so the fact that the bankers involved knew or should have known that they were making a false rep and warranty was indisputable.

The result of the brazen nature of the piggy-back mortgage fraud – a fraud that was certain to be uncovered frequently because it would lead to much higher default rates – was that the lenders and underwriters were on the hook for these losses. Because they made blatantly false representations they would be forced contractually to repurchase the defaulting the piggy-back loans. Worse, they could be sued in tort for fraud, which might well lead to the imposition of punitive damages and the ability to put back the entire purchase to the seller.

Making a “rep and warranty” that there is no second lien when the lender has made a simultaneous piggy-back first and second lien loan is a far more brazen fraud than appraisal and “liar’s” loan frauds because the lender has knowledge of a vital, objective fact – and deliberately misrepresents the fact in a manner harmful to the purchaser. The PSW findings about fraudulent piggy-back loans demonstrate that there is no basis for assuming that the same elite bankers would not have knowingly and intentionally have engaged in mortgage fraud in other contexts in which it would be far more difficult for the loan, MBS, or CDO purchaser to establish a contractual right to “put back” the loan or sue for tort relief.

We know from the PSW study that our most elite bankers were willing to engage in piggy-back frauds that were so brazen that they were sure to be discovered in large numbers of cases and lead to huge losses to the elite banks. The logical inference is that the same elite bank officers would be far more willing to engage in other forms of fraudulent reps and warranties that were far harder for the victim, regulators, and prosecutors to discover and sanction.

The Fundamental Unaddressed Question: Why?

The fundamental question, however, was not addressed by the PSW study – why did the officers controlling the lenders deliberately make terrible piggy-back loans that we have known for a century will produce much higher default rates and losses? The authors know that the answer is not “the lenders had no skin in the game” because they were selling the loans to the secondary market. The PSW authors know that the fraudulently originated loans could only be sold to the secondary market through fraudulent reps and warranties and that this meant that the loan originators had serious-to-fatal levels of skin in the game.

The more subtle, but even more important “why” question is: what has changed to produce a vastly more criminogenic environment, particularly in the U.S. and the EU? Decades ago, if a bank made terrible loans that would cause it to suffer catastrophic losses it created no Gresham’s” dynamic. Changes in executive compensation created an intense Gresham’s dynamic that now creates perverse incentives for bank managers to cause “their” banks to make enormous numbers of bad loans.

The Missing Literature that Explains Why

The PSW authors were not aware, however, of the answers to these fundamental questions provided by the criminology, regulatory, and economics literature, such as the creation of an environment that is so criminogenic that it creates a powerful incentive for the banks’ controlling officers to make vast amounts of bad loans. Our analysis differs critically from the PSW authors’ understanding of fraud by lenders.

“These misrepresentations are not instances of the classic asymmetric information problem in which the buyers know less than the seller. Rather, we contend that they are instances where, in the process of contractual disclosure by the sellers, buyers received false information on the characteristics of assets. (PSW: 1).”The use of the word “classic” indicates an important (retrograde) movement in economics. The “classic” treatment of asymmetry in the economics literature is George Akerlof’s 1970 article on a market for “lemons.” It is all about “buyers receiv[ing] false information on the characteristics of assets” in the process of “contractual disclosure by the sellers.” Akerlof presented a dynamic process in which the seller makes false disclosures as to the quality of its goods in order to maximize the asymmetry of information with the borrower and aid the seller in defrauding the borrower. Fraud maximizes the asymmetry between the buyer and the seller. Indeed, Akerlof emphasized the propagation of that fraudulent asymmetry through the industry as a result of what he dubbed a “Gresham’s” dynamic.

“[D]ishonest dealings tend to drive honest dealings out of the market. The cost of dishonesty, therefore, lies not only in the amount by which the purchaser is cheated; the cost also must include the loss incurred from driving legitimate business out of existence “(Akerlof 1970).The fact that top economists, 40 years later, claimed that fraud does not represent a “classic” pathology of asymmetrical information demonstrates how far economics has fallen. Criminologists and competent regulators have recognized since Akerlof’s classic article that countering the Gresham’s dynamic is the paramount function of the rule of law and regulation.

The PSW authors (as with the other three co-authored articles I will discuss in this series) cite none of the relevant criminology or regulatory literature, which is of course the norm for economists. But they also cite neither Akerlof (1970) nor Akerlof and Romer (1993), the seminal economics article about lending fraud (“Looting: The Economic Underworld of Bankrutpcy for Profit”). Akerlof and Romer drew on the literature, theories, and data of effective regulators (which incorporated criminology) in developing their theory of “looting.”

In no other discipline would you find a Nobel Laureate who has authored the two most important theoretical articles in the discipline about a subject (fraud in this case) ignored by scholars from that same field. In future articles in this series I will explain how the relevant literature answers the “why” questions in greater detail. For now, I will simply issue the “spoiler” – because, given modern executive compensation, the “fraud recipe” is optimized by making (and buying) terrible loans at premium nominal yield.

The fraud recipe produces the three “sure things” that make those officers wealthy while minimizing the risk of prosecution. PSW help illustrate the fact that this hard-gained knowledge disappeared from the ken of financial economists and regulators – but not from bank officers. George Akerlof and Paul Romer proved vastly too optimistic about economists and economics in the conclusion to their famous 1993 article “Looting: The Economic Underworld of Bankruptcy for Profit.”

“The S&L crisis, however, was also caused by misunderstanding. Neither the public nor economists foresaw that the [deregulations] of the 1980s were bound to produce looting. Nor, unaware of the concept, could they have known how serious it would be. Thus the regulators in the field who understood what was happening from the beginning found lukewarm support, at best, for their cause. Now we know better. If we learn from experience, history need not repeat itself” (Akerlof & Romer 1993: 60).The Dog That Didn’t Bark: The Lack of Federal Regulatory Studies of Mortgage Fraud

We also need to emphasize the dog that has not barked – the federal financial regulators, the bankruptcy trustees, and the FBI. They have unique access to data that would allow superb studies of the role of fraud in the crisis. I have called on them (publicly and privately) for many years to conduct the studies. Our “autopsies” of failed S&Ls provided the data essential to our ability to understand the “fraud recipe” and how the lenders’ controlling officers generated the Gresham’s dynamics that suborned the purported “controls” into becoming the most valuable fraud allies.

The federal and state regulatory and criminal justice agencies have found endemic fraud at our most elite financial institutions – but the federal government’s most senior officials, President Obama and Attorney General Holder, are fraud deniers. If the regulatory agencies, bankruptcy trustees, and the FBI used their resources, including their unique access to data and examination powers, to study mortgage fraud in the origination and secondary (and tertiary, e.g., CDOs) markets they could have documented and acted decisively to end the fraud epidemics a full decade ago and prevented the crisis.

In addition to examination reports, the regulators, federal bankruptcy trustees, and the FBI have unique ability to investigate non-regulated entities and actors, locate and learn from whistleblowers, require detailed admissions from the banks when they reach civil settlements and criminal pleas, require the banks to pay for experts chosen by DOJ to conduct detailed, truly independent investigations of the fraud schemes, conduct intensive bankruptcy trustee investigations, and the Clayton materials.

The Clayton materials, in particular, are a treasure trove for research. (Clayton was the dominant “due diligence” firm for secondary market mortgage purchasers. The due diligence reports from the less than handful of material competitors would also prove highly valuable. The FBI and the DOJ should be commissioning in depth analyses using the Clayton data – and documenting through the many Clayton whistleblowers the nature and extent of the efforts to ensure that the Clayton reports substantially underreported the incidence of false “reps and warranties.” Similarly, the instructions that Clayton received from the secondary market purchasers and the responses from those purchasers to the extraordinary levels of false reps and warranties found by Clayton would be highly incriminating and vital to researchers.

The continuing refusal of the federal banking regulatory agencies, the failure to appoint bankruptcy trustees and resultant failure to conduct bankruptcy examinations of notorious lenders like GreenPoint, and the FBI and DOJ’s failures to conduct major studies of mortgage fraud are indefensible. They should be putting together research teams of criminologists, effective (former) regulators, and economists with funding and access to the data to conduct these studies. The current crisis is so horrific in the damage it has inflicted that the failure of the federal government to conduct superb mortgage fraud studies is incomprehensible.

In subsequent articles in this series I will discuss two studies of liar’s loans by Federal Reserve economists as sole or co-authors. Neither study was done on behalf of the Federal Reserve. Neither study took advantage of the regulators’, FBI and DOJ’s, and bankruptcy examiners’ unique access to institution-specific data. Neither study involved co-authorship by actual regulators. Neither study gives any indication of regulatory or prosecutorial insights. Neither study cites Akerlof’s articles or any of the literature of criminologists or effective banking regulators. This helps explain why both studies are embarrassingly weak. They are credulous in accepting industry characterizations of liar’s loans. Neither study discusses fraud. Only one of the studies even contains the word “fraud” – and the single use of the word is relegated to a quotation in a footnote that the authors do not analyze.

Good Data on Mortgage Fraud Would Embarrass DOJ’s Leaders

Real federal research on mortgage fraud poses two dangers to the Department of Justice (DOJ), which should have been publicly demanding that the regulators conduct superb fraud studies. The first danger is obvious. There is no excuse for the DOJ’s continuing refusal to prosecute the elite bankers (the fraud “lions” the regulators allowed to roam the campsite with impunity) who led the frauds that drove the crisis. Any serious research effort by the financial regulators would make that outrage even clearer.

The more subtle problem is that while DOJ refuses to prosecute elite bankers, it does annually chase hundreds of the fraud “mice” into prison. As we demonstrated in the Sacramento mortgage fraud defense, the facts disclosed by every relevant study and investigation of mortgage fraud demonstrate that the loan application misrepresentations were not “material” (a necessary legal element to demonstrate fraud in federal prosecutions) to the typical originators (and purchasers) of fraudulent liar’s loans.

DOJ views these facts as the gravest threat to its prosecution of the purported fraud mice. DOJ routinely portrays to juries that lenders it knows to have engaged in endemic loan origination fraud are the innocent victims of the rapacious and endlessly clever hairdressers. That fable would be impossible to spread – and use to send the mice to prison – if the regulators had published studies demonstrating that the originators of liar’s loans were frauds. I have also explained how the FBI compounds the outrageous nature of that fable by falsely claiming on its web site that mortgage fraud is widely driven by disfavored ethnic groups.

PSW put the conclusive lie to the clever hairdresser fable about the causes of the crisis two years ago when their study was made public in February 2013.

'Rotten Core of Banking' Exposed: Global Outrage Follows HSBC Revelations

'These bankers are too big to fail and too big to jail, so they just keep engaging in illegal activity.'

"It's time we ensured banks were working in the public's interest instead of conspiring against us," says David Hillman of the Robin Hood Tax campaign. (Photo: Gyver Chang/flickr/cc)

New details about how HSBC bank helped tax evaders and money-launderers—from political figures to celebrities to arms dealers—conceal billions of dollars in assets have sparked international condemnation, from elected officials as well as public interest groups around the world.

Documents leaked by whistleblower Hervé Falciani, who worked for HSBC, show how a Swiss division of the U.K.-headquartered bank routinely allowed clients to withdraw bricks of cash, often in foreign currencies of little use in Switzerland; aggressively marketed schemes likely to enable wealthy clients to avoid European and U.S. taxes; colluded with some clients to conceal undeclared "black" accounts from their domestic tax authorities; and provided accounts to international criminals, corrupt businessmen, and other high-risk individuals.

"This exposes once again the rotten core of banking—it would be shocking if it weren't for the frequency with which we hear of such scandals," said David Hillman, spokesperson for the U.K.-based Robin Hood Tax campaign. "It shows a sector not content with dodging its own obligations, but also conniving to help the richest people shirk their responsibilities to society as well."

"It's clear our...approach to the banking sector is wholly inadequate," Hillman continued.

"It's time we ensured banks were working in the public's interest instead of conspiring against us."

James Henry, former chief economist at the international consultancy firm McKinsey & Co. and now senior adviser with the U.K.'s Tax Justice Network, noted that HSBC got hit with a $1.9 billion fine for sanctions-busting and money-laundering in 2012, "but only a $12 million fine from the SEC related to this tax dodging." Regardless, such fines do little to change systemic corruption, he said.

"These bankers are too big to fail and too big to jail, so they just keep engaging in illegal activity," Henry declared. "There’s a widespread pattern of using fines to penalize the top 20 global big banks — $247 billion since 1998, for 655 separate major infractions of all kinds. But they just pass along the costs and continue with business as usual, with client secrecy preserved. It’s like a criminal syndicate."

In the U.S., Sen. Sherrod Brown (D-Ohio) called on the federal government to explain "its actions — or lack thereof — upon learning of these allegations in 2010." The Guardian established that the leaked data was shared with U.S. regulators five years ago.

Meanwhile, Jack Blum, a former tax investigator at the U.S. Senate, said on 60 Minutes Sunday evening that any bank that helped an American citizen to evade taxes was guilty of a felony.

"First of all, for the average American taxpayer it's beyond shocking," he said. "But, perhaps, not that surprising. Swiss banks have been caught protecting tax dodgers before, but never has this much detail been revealed. Under U.S. law, any bank that does that, that assists a U.S. person in evading U.S. tax is guilty of a felony. And it doesn't matter where the bank is located or where the bankers are located."

Meanwhile, In China There's a Stock Market Crash

Wednesday, July 08, 2015

No Jobs for the Young, No Retirement for the Old

We shouldn't wonder why people are working into their 70s - we should wonder why anyone retires, assuming they'll still be receiving their full pension in five years.

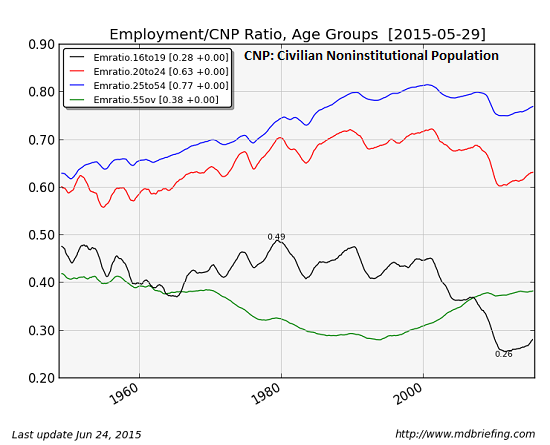

You may have seen a variation of this chart of employment in the U.S. by age group. This chart--courtesy of mdbriefing.com - shows the number of those employed (with any kind of job - full-time, part-time, self-employed) as a percentage of the Civilian Noninstitutional Population (CNP), which includes everyone 16 years of age and older who is not institutionalized or on active duty in the Armed Forces. (Click on link to enlarge chart.)

A number of striking features pop out of this chart:

1. Employment in the 16-19 age cohort has been dropping for 35 years, and fell off a cliff in 2008.

2. Employment in the 20-24 and 25-54 age cohorts topped out in 2001 and has yet to recover the pre-recession levels of 2008.

3. The only age cohort with employment growth since 2000 is the 55 and older group.

There are many theories as to why youth employment has plummeted while 55+ employment is rising, but demographics and financial insecurity likely play major roles. Back when Social Security was established, few people lived beyond their 60s. A retirement age of 65 meant most people lived only a few years beyond retirement.

Now people live into their 80s, and medical technologies are enabling many to remain active even in their advanced years.

As people live longer, those reaching retirement age (early to mid 60s) often have elderly parents in their 80s who need care and financial support. People living into their late 80s, once a rarity, are now commonplace.

As the economy has stagnated, financial demands on their own children (in their 30s and early 40s) have increased, leaving many of those reaching retirement age with two generations needing help. Retirement is not much of an option when every scrap of income is needed.

Over the past 35 years, defined pension plans that were once common benefits of corporate employment have vanished and been replaced by 401K plans which transfer the risk to the employee. As the stock market has soared and crashed twice in the past fifteen years, those approaching retirement can no longer trust that their pension fund is secure.

The Federal Reserve's Zero Interest Rate Policy (ZIRP) has destroyed low-risk yields on retirement funds (401Ks, IRAs, etc.), greatly reducing the yield on retirement savings. As a a direct result of Fed policy (designed to recapitalize banks at the expense of savers and retirees), those hoping to retire have been forced to put their savings at risk (investing in risky assets such as junk bond funds) or working longer because the low-risk yield on retirement savings are now meager.

The reality is that financial insecurity is rising for everyone heading into retirement. Even state and local government workers are concerned that their pensions aren't as secure as they were a generation or two ago, as the fiscal imbalances of many local government budgets are the New Normal.

The Federal government can effectively create money to pay Social Security, veterans and federal employee pensions, but there is no guarantee that these pensions will keep up with inflation or not be taxed to oblivion. One key source of financial insecurity is the growing awareness that the rules will be changed without consent of the governed to preserve the perquisites of the Ruling Class and powerful vested interests.

It would be foolish in the extreme to trust that the Powers That Be won't change the rules in a heartbeat when their power and wealth are threatened by instability. The Nobility will change the rules and the peasants will pay - end of story.

In this context, we shouldn't wonder why people are working into their 70s - we should wonder why anyone retires, assuming they'll still be receiving their full pension in five years.

No comments:

Post a Comment