(Please consider making a contribution to the Welcome to Pottersville2 Holiday Season Fundraiser or at least sending a link to your friends if you think the subjects discussed here are worth publicizing. Thank you for your support. We are in a real tight spot financially right now and would sincerely appreciate any type of contribution. Anything you can do will make a huge difference in this blog's ability to survive.)

John Kenneth Galbraith said, “The sense of responsibility in the financial community for the community as a whole is not small. It is nearly nil.”

It's not only nearly nil, it's self-aggrandizing, oily and mendacious as well.

Saturday, Nov 30, 2013

Sorry, Neoliberals: Inequality Is Driven by Greed, Not Technology

A new study shows low wages are really caused by low minimum wage, weakened unions and the effects of globalization

Sean McElwee

Billionaire Tom Friedman pretends to feel empathy for poor people as he writes columns for The New York Times decrying their ignorance, stupidity and unluckiness.

Inequality may be the greatest economic challenge of our generation. Yet despite extensive academic debate, there is still no consensus as to its causes. Earlier this year, Tyler Cowen sparked a debate on the subject with his book Average is Over, in which he argues that inequality is driven by new developments in technology that give some workers who can capably use the technology a wage premium over those who can’t. Future innovations in technology, he argues, will contribute to hyper-meritocracy and further inequality.

. . . The problem, then, is not machines, which are doing a great deal to boost productivity; the problem is that the benefits from increased productivity no longer accrue to workers. In a provocative paper earlier this year, Josh Bivens and Mishel argued that the gains for the richest 1 percent were due to “rent-seeking” behavior by CEOs and financial professions, not competitive markets. As John Kenneth Galbraith said, “The sense of responsibility in the financial community for the community as a whole is not small. It is nearly nil.”

The newly minted rich want to blame robots for declining wages at the bottom and their innate superiority for their disproportionate share of the income. But these excuses mask their theft of productivity gains that rightfully belong to the rest of us.

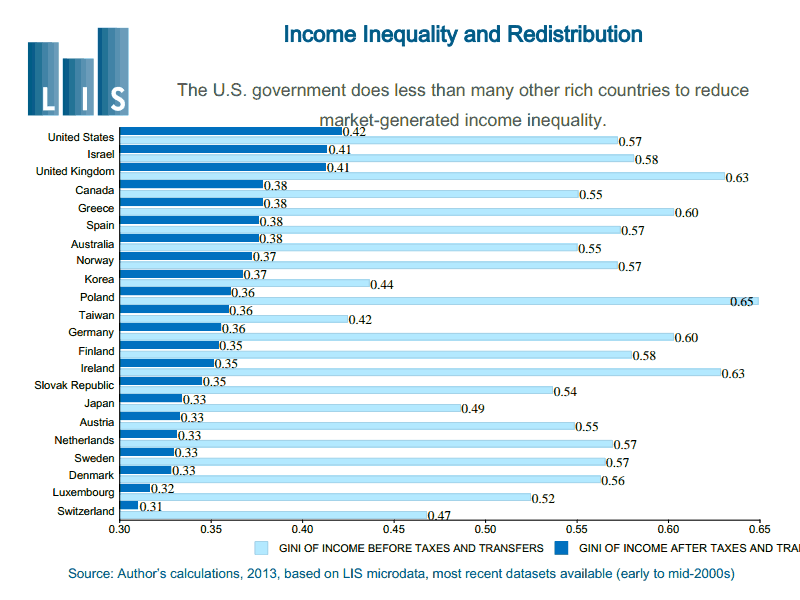

If inequality were inevitable, as many on the right believe, we would expect to see inequality rising internationally. But, in truth, different societies have responded to inequality in different ways. I talked to Janet Gornick, professor at the Graduate Center at CUNY and director of Luxembourg Income Study Center, about her work in the field of inequality.

She tells me that “these transnational factors matter — globalization, technological change, neoliberal reforms — but what matters, perhaps more, is national-level policies and institutions. What is our evidence for that? Stark variation across relatively similar countries.” She tells me that some two-thirds of OECD countries have faced rising levels of inequality, however “the increase in inequality in OECD countries has been modest. The rise in the U.S. has been greater; there is something clearly going on at that national level, that is absolutely certain.”

This chart should wake you up and encourage you to start reading graphs more carefully from now on.

If inequality were the result of economic fundamentals, it would not matter who was in the White House, but rather inequality would be correlated to underlying economic trends. This is not true either. Larry Bartels finds in “Unequal Democracy” that income growth is more equal under Democratic presidents than it is under Republican presidents, pointing to the possibility that political systems drive inequality._ _ _ _ _ _ _

Since inequality is “man-made,” it can be ameliorated by changing our institutions. As Mishel said, “My interpretation that the outcomes we see are the products of policy decisions made or not made — not raising the minimum wage, not reforming labor law — is optimistic. We have it in our power to shape the future.”

A recent article by Harold Meyerson in the American Prospect echoes this sentiment: “The extinction of a large and vibrant American middle class isn’t ordained by the laws of either economics or physics. Many of the impediments to creating anew a broadly prosperous America are ultimately political creations that are susceptible to political remedy.”

Blaming technology is an excuse to abdicate responsibility. Calling for more education and upward mobility, while noble, is useless when wages are falling for college graduates and will still leave many workers behind. Social mobility is good, but it shouldn’t supplant the goal of reducing inequality (and it’s unlikely that high levels of upward mobility can co-exist with rampant inequality).

As Terry Eagleton writes in “Across the Pond,” “As long as you have enough willpower and ambition, the fact that you are a destitute Latino with a gargantuan drink problem puts you at no disadvantage to graduates of the Harvard Business School when it comes to scaling the social ladder. All you need to do is try.”

Workers must exercise political power to change the institutions that shape their lives. Walmart doesn’t have to pay its workers starvation wages and could easily pay them more. There is no celestial law that the richest 1% can plunder our common inheritance.

We don’t have to crush workers when we globalize and we don’t have to destroy the environment in the pursuit of profits. Just as inequality is a choice, equality is a choice. By shifting the discussion away from the policy changes that have caused inequality, we legitimate it. As Eugene Debs said, “the class which has the power to rob upon a large scale has also the power to control the government and legalize their robbery.”

Sean McElwee is a writer and researcher of public policy. His writing may be viewed at seanamcelwee.com. Follow him on Twitter at @seanmcelwee.

Did you have much trouble while trying to interpret Larry Summers' latest seppuku, er . . . maze, labyrinthal sudoku, or Seven Bridges of Königsberg desperately needed money fix for the banksters?

Dr. Paul Craig Roberts didn't.

When a person becomes a Treasury official it is made clear that the choice is between serving the banks and becoming rich or trying to serve the public and becoming poor. Few make the latter choice.

As Michael Hudson has informed us, the goal of the financial sector has always been to convert all income, from corporate profits to government tax revenues, to the service of debt. From the bankers standpoint, the more debt the richer the bankers. Rubin, Summers, Paulson, Geithner, and now banker Treasury Secretary Jack Lew faithfully serve this goal.

The Federal Reserve describes its policy of Quantitative Easing — the creation of new money with which the Fed purchases Treasury debt and mortgage backed securities — as a low interest rate policy in order to stimulate employment and economic growth. Economists and the financial media have parroted this cover story.

In contrast, I have exposed QE as a scheme for pumping profits into the banks and boosting their balance sheets. The real purpose of QE is to drive up the prices of the debt-related derivatives on the banks’ books, thus keeping the banks with solvent balance sheets.

Writing in the Wall Street Journal (“Confessions of a Quantitative Easer,” November 11, 2013), Andrew Huszar confirms my explanation to be the correct one. Huszar is the Federal Reserve official who implemented the policy of QE. He resigned when he realized that the real purpose of QE was to drive up the prices of the banks’ holdings of debt instruments, to provide the banks with trillions of dollars at zero cost with which to lend and speculate, and to provide the banks with “fat commissions from brokering most of the Fed’s QE transactions.” (See: www.paulcraigroberts.org )

This vast con game remains unrecognized by Congress and the public. At the IMF Research Conference on November 8, 2013, former Treasury Secretary Larry Summers presented a plan to expand the con game.

Summers says that it is not enough merely to give the banks interest free money. More should be done for the banks. Instead of being paid interest on their bank deposits, people should be penalized for keeping their money in banks instead of spending it.

To sell this new rip-off scheme, Summers has conjured up an explanation based on the crude and discredited Keynesianism of the 1940s that explained the Great Depression as a problem caused by too much savings. Instead of spending their money, people hoarded it, thus causing aggregate demand and employment to fall.

Summers says that today the problem of too much saving has reappeared. The centerpiece of his argument is “the natural interest rate,” defined as the interest rate at which full employment is established by the equality of saving with investment. If people save more than investors invest, the saved money will not find its way back into the economy, and output and employment will fall.

Summers notes that despite a zero real rate of interest, there is still substantial unemployment. In other words, not even a zero rate of interest can reduce saving to the level of investment, thus frustrating a full employment recovery. Summers concludes that the natural rate of interest has become negative and is stuck below zero.

How to fix this? The way to fix it, Summers says, is to charge people for saving money. To avoid the charges, people would spend the money, thus reducing savings to the level of investment and restoring full employment.

>Summers acknowledges that the problem with his solution is that people would take their money out of banks and hoard it in cash holdings. In other words, the cash form of money provides consumers with a freedom to save that holds down consumption and prevents full employment.

Summers has a fix for this: eliminate the freedom by imposing a cashless society where the only money is electronic. As electronic money cannot be hoarded except in bank deposits, penalties can be imposed that force unproductive savings into consumption.

Summers’ scheme, of course, is a harebrained one. With governments running huge deficits, who would purchase bonds at negative interest rates? How would pension and retirement funds operate? Would they also be subject to an annual percentage confiscation?

We know that the response of consumers to the long term decline in real median family income, to the loss of jobs from labor arbitrage across national borders (jobs offshoring), to rising homelessness, to cuts in the social safety net, to the transformation of their full time jobs to part time jobs (employers’ response to Obamacare), has been to reduce their savings rate.

Indeed, few have any savings at all. The US personal saving rate is currently 2 percentage points, about 30%, below the long term average. Retired people, unable to earn any interest on their savings from the Fed’s zero interest rate policy, are being forced to draw down their savings in order to pay their bills.

Moreover, it is unclear whether the savings rate is an accurate measure or merely a residual of other calculations. With so many people having to draw down their savings, I wouldn’t be surprised if an accurate measure showed the personal savings rate to be negative.

But for Summers the plight of the consumer is not the problem. The problem is the profits of the banks. Summers has the solution, and the establishment, including Paul Krugman, is applauding it. Once the economy officially turns down again, watch out.

This column first appeared as a Trend Alert, Trends Research Institute

It's almost funny, isn't it? The banks refuse to lend to mere consumers (not enough profit there, you know) unless it's the new subprime car loans, but want to penalize us for actually putting money in their rip-off banks and then not spending it fast enough. So much for Economics 101.

No comments:

Post a Comment