Lots of fake gasps from the worldclass fakers?

The world rejoices at the signing of the latest nuclear treaty as the U.S. and its allies, Israel and Saudi Arabia feign horrification.

The one candidate with some foreign policy experience, Lindsey Graham, describes the deal as "a death sentence for the state of Israel," which will certainly come as a surprise to Israeli intelligence and strategic analysts - and which Graham knows to be utter nonsense, raising immediate questions about actual motives.

Keep in mind that the Republicans long ago abandoned the pretense of functioning as a normal congressional party. They have, as respected conservative political commentator Norman Ornstein of the right-wing American Enterprise Institute observed, become a "radical insurgency" that scarcely seeks to participate in normal congressional politics.

Since the days of President Ronald Reagan, the party leadership has plunged so far into the pockets of the very rich and the corporate sector that they can attract votes only by mobilizing parts of the population that have not previously been an organized political force. Among them are extremist evangelical Christians, now probably a majority of Republican voters; remnants of the former slave-holding states; nativists who are terrified that "they" are taking our white Christian Anglo-Saxon country away from us; and others who turn the Republican primaries into spectacles remote from the mainstream of modern society - though not from the mainstream of the most powerful country in world history.

The departure from global standards, however, goes far beyond the bounds of the Republican radical insurgency. Across the spectrum, there is, for instance, general agreement with the "pragmatic" conclusion of General Martin Dempsey, chairman of the Joint Chiefs of Staff, that the Vienna deal does not "prevent the United States from striking Iranian facilities if officials decide that it is cheating on the agreement," even though a unilateral military strike is "far less likely" if Iran behaves.

. . . Israel, of course, is one of the three nuclear powers, along with India and Pakistan, whose weapons programs have been abetted by the United States and that refuse to sign the Nonproliferation Treaty (NPT).

. . . Repeatedly, implementation of the resolution has been blocked by the U.S., most recently by President Obama in 2010 and again in 2015, as Dhanapala and Duarte point out, "on behalf of a state that is not a party to the NPT and is widely believed to be the only one in the region possessing nuclear weapons" - a polite and understated reference to Israel. This failure, they hope, "will not be the coup de grâce to the two longstanding NPT objectives of accelerated progress on nuclear disarmament and establishing a Middle Eastern WMD-free zone."

A nuclear-weapons-free Middle East would be a straightforward way to address whatever threat Iran allegedly poses, but a great deal more is at stake in Washington's continuing sabotage of the effort in order to protect its Israeli client. After all, this is not the only case in which opportunities to end the alleged Iranian threat have been undermined by Washington, raising further questions about just what is actually at stake.

In considering this matter, it is instructive to examine both the unspoken assumptions in the situation and the questions that are rarely asked. Let us consider a few of these assumptions, beginning with the most serious: that Iran is the gravest threat to world peace.

In the U.S., it is a virtual cliché among high officials and commentators that Iran wins that grim prize. There is also a world outside the U.S. and although its views are not reported in the mainstream here, perhaps they are of some interest. According to the leading western polling agencies (WIN/Gallup International), the prize for "greatest threat" is won by the United States. The rest of the world regards it as the gravest threat to world peace by a large margin. In second place, far below, is Pakistan, its ranking probably inflated by the Indian vote.

. . . Turning to the next obvious question, what in fact is the Iranian threat? Why, for example, are Israel and Saudi Arabia trembling in fear over that country?

Whatever the threat is, it can hardly be military. Years ago, U.S. intelligence informed Congress that Iran has very low military expenditures by the standards of the region and that its strategic doctrines are defensive - designed, that is, to deter aggression. The U.S. intelligence community has also reported that it has no evidence Iran is pursuing an actual nuclear weapons program and that "Iran's nuclear program and its willingness to keep open the possibility of developing nuclear weapons is a central part of its deterrent strategy."

. . . The authoritative SIPRI review of global armaments ranks the U.S., as usual, way in the lead in military expenditures. China comes in second with about one-third of U.S. expenditures. Far below are Russia and Saudi Arabia, which are nonetheless well above any western European state. Iran is scarcely mentioned. Full details are provided in an April report from the Center for Strategic and International Studies (CSIS), which finds "a conclusive case that the Arab Gulf states have... an overwhelming advantage of Iran in both military spending and access to modern arms."

Iran's military spending, for instance, is a fraction of Saudi Arabia's and far below even the spending of the United Arab Emirates (UAE). Altogether, the Gulf Cooperation Council states - Bahrain, Kuwait, Oman, Saudi Arabia, and the UAE - outspend Iran on arms by a factor of eight, an imbalance that goes back decades. The CSIS report adds: "The Arab Gulf states have acquired and are acquiring some of the most advanced and effective weapons in the world [while] Iran has essentially been forced to live in the past, often relying on systems originally delivered at the time of the Shah." In other words, they are virtually obsolete.

When it comes to Israel, of course, the imbalance is even greater. Possessing the most advanced U.S. weaponry and a virtual offshore military base for the global superpower, it also has a huge stock of nuclear weapons.

To be sure, Israel faces the "existential threat" of Iranian pronouncements: Supreme Leader Khamenei and former president Mahmoud Ahmadinejad famously threatened it with destruction. Except that they didn't - and if they had, it would be of little moment. Ahmadinejad, for instance, predicted that "under God's grace [the Zionist regime] will be wiped off the map." In other words, he hoped that regime change would someday take place.

Even that falls far short of the direct calls in both Washington and Tel Aviv for regime change in Iran, not to speak of the actions taken to implement regime change. These, of course, go back to the actual "regime change" of 1953, when the U.S. and Britain organized a military coup to overthrow Iran's parliamentary government and install the dictatorship of the Shah, who proceeded to amass one of the worst human rights records on the planet.

No serious analyst believes that Iran would ever use, or even threaten to use, a nuclear weapon if it had one, and so face instant destruction. There is, however, real concern that a nuclear weapon might fall into jihadi hands - not thanks to Iran, but via U.S. ally Pakistan. In the journal of the Royal Institute of International Affairs, two leading Pakistani nuclear scientists, Pervez Hoodbhoy and Zia Mian, write that increasing fears of "militants seizing nuclear weapons or materials and unleashing nuclear terrorism [have led to] ... the creation of a dedicated force of over 20,000 troops to guard nuclear facilities. There is no reason to assume, however, that this force would be immune to the problems associated with the units guarding regular military facilities," which have frequently suffered attacks with "insider help." In brief, the problem is real, just displaced to Iran thanks to fantasies concocted for other reasons.

Other concerns about the Iranian threat include its role as "the world's leading supporter of terrorism," which primarily refers to its support for Hezbollah and Hamas. Both of those movements emerged in resistance to U.S.-backed Israeli violence and aggression, which vastly exceeds anything attributed to these villains, let alone the normal practice of the hegemonic power whose global drone assassination campaign alone dominates (and helps to foster) international terrorism.

Those two villainous Iranian clients also share the crime of winning the popular vote in the only free elections in the Arab world. Hezbollah is guilty of the even more heinous crime of compelling Israel to withdraw from its occupation of southern Lebanon, which took place in violation of U.N. Security Council orders dating back decades and involved an illegal regime of terror and sometimes extreme violence. Whatever one thinks of Hezbollah, Hamas, or other beneficiaries of Iranian support, Iran hardly ranks high in support of terror worldwide.

. . . Another concern, voiced at the U.N. by U.S. Ambassador Samantha Power, is the "instability that Iran fuels beyond its nuclear program." The U.S. will continue to scrutinize this misbehavior, she declared. In that, she echoed the assurance Defense Secretary Ashton Carter offered while standing on Israel's northern border that "we will continue to help Israel counter Iran's malign influence" in supporting Hezbollah, and that the U.S. reserves the right to use military force against Iran as it deems appropriate.

The way Iran "fuels instability" can be seen particularly dramatically in Iraq where, among other crimes, it alone at once came to the aid of Kurds defending themselves from the invasion of Islamic State militants, even as it is building a $2.5 billion power plant in the southern port city of Basra to try to bring electrical power back to the level reached before the 2003 invasion.

Ambassador Power's usage is, however, standard: Thanks to that invasion, hundreds of thousands were killed and millions of refugees generated, barbarous acts of torture were committed - Iraqis have compared the destruction to the Mongol invasion of the thirteenth century - leaving Iraq the unhappiest country in the world according to WIN/Gallup polls. Meanwhile, sectarian conflict was ignited, tearing the region to shreds and laying the basis for the creation of the monstrosity that is ISIS. And all of that is called "stabilization."

Only Iran's shameful actions, however, "fuel instability." The standard usage sometimes reaches levels that are almost surreal, as when liberal commentator James Chace, former editor of "Foreign Affairs," explained that the U.S. sought to "destabilize a freely elected Marxist government in Chile" because "we were determined to seek stability" under the Pinochet dictatorship.

Others are outraged that Washington should negotiate at all with a "contemptible" regime like Iran's with its horrifying human rights record and urge instead that we pursue "an American-sponsored alliance between Israel and the Sunni states." So writes Leon Wieseltier, contributing editor to the venerable liberal journal the Atlantic, who can barely conceal his visceral hatred for all things Iranian. With a straight face, this respected liberal intellectual recommends that Saudi Arabia, which makes Iran look like a virtual paradise, and Israel, with its vicious crimes in Gaza and elsewhere, should ally to teach that country good behavior. Perhaps the recommendation is not entirely unreasonable when we consider the human rights records of the regimes the U.S. has imposed and supported throughout the world.

It might also be useful to recall - surely Iranians do - that not a day has passed since 1953 in which the U.S. was not harming Iranians. After all, as soon as they overthrew the hated U.S.-imposed regime of the Shah in 1979, Washington put its support behind Iraqi leader Saddam Hussein, who would, in 1980, launch a murderous assault on their country.

President Reagan went so far as to deny Saddam's major crime, his chemical warfare assault on Iraq's Kurdish population, which he blamed on Iran instead. When Saddam was tried for crimes under U.S. auspices, that horrendous crime, as well as others in which the U.S. was complicit, was carefully excluded from the charges, which were restricted to one of his minor crimes, the murder of 148 Shi'ites in 1982, a footnote to his gruesome record.

Saddam was such a valued friend of Washington that he was even granted a privilege otherwise accorded only to Israel. In 1987, his forces were allowed to attack a U.S. naval vessel, the USS Stark, with impunity, killing 37 crewmen. (Israel had acted similarly in its 1967 attack on the USS Liberty.) Iran pretty much conceded defeat shortly after, when the U.S. launched Operation Praying Mantis against Iranian ships and oil platforms in Iranian territorial waters. That operation culminated when the USS Vincennes, under no credible threat, shot down an Iranian civilian airliner in Iranian airspace, with 290 killed - and the subsequent granting of a Legion of Merit award to the commander of the Vincennes for "exceptionally meritorious conduct" and for maintaining a "calm and professional atmosphere" during the period when the attack on the airliner took place.

Comments philosopher Thill Raghu, "We can only stand in awe of such display of American exceptionalism!"

After the war ended, the U.S. continued to support Saddam Hussein, Iran's primary enemy. President George H.W. Bush even invited Iraqi nuclear engineers to the U.S. for advanced training in weapons production, an extremely serious threat to Iran. Sanctions against that country were intensified, including against foreign firms dealing with it, and actions were initiated to bar it from the international financial system.

In recent years the hostility has extended to sabotage, the murder of nuclear scientists (presumably by Israel), and cyberwar, openly proclaimed with pride. The Pentagon regards cyberwar as an act of war, justifying a military response, as does NATO, which affirmed in September 2014 that cyber attacks may trigger the collective defense obligations of the NATO powers - when we are the target that is, not the perpetrators.

. . . It is only fair to add that there have been breaks in this pattern. President George W. Bush, for example, offered several significant gifts to Iran by destroying its major enemies, Saddam Hussein and the Taliban. He even placed Iran's Iraqi enemy under its influence after the U.S. defeat, which was so severe that Washington had to abandon its officially declared goals of establishing permanent military bases ("enduring camps") and ensuring that U.S. corporations would have privileged access to Iraq's vast oil resources.

Do Iranian leaders intend to develop nuclear weapons today? We can decide for ourselves how credible their denials are, but that they had such intentions in the past is beyond question. After all, it was asserted openly on the highest authority and foreign journalists were informed that Iran would develop nuclear weapons "certainly, and sooner than one thinks." The father of Iran's nuclear energy program and former head of Iran's Atomic Energy Organization was confident that the leadership's plan "was to build a nuclear bomb." The CIA also reported that it had "no doubt" Iran would develop nuclear weapons if neighboring countries did (as they have).

All of this was, of course, under the Shah, the "highest authority" just quoted and at a time when top U.S. officials - Dick Cheney, Donald Rumsfeld, and Henry Kissinger, among others - were urging him to proceed with his nuclear programs and pressuring universities to accommodate these efforts. Under such pressures, my own university, MIT, made a deal with the Shah to admit Iranian students to the nuclear engineering program in return for grants he offered and over the strong objections of the student body, but with comparably strong faculty support (in a meeting that older faculty will doubtless remember well).

Asked later why he supported such programs under the Shah but opposed them more recently, Kissinger responded honestly that Iran was an ally then.

Putting aside absurdities, what is the real threat of Iran that inspires such fear and fury? A natural place to turn for an answer is, again, U.S. intelligence. Recall its analysis that Iran poses no military threat, that its strategic doctrines are defensive, and that its nuclear programs (with no effort to produce bombs, as far as can be determined) are "a central part of its deterrent strategy."

Who, then, would be concerned by an Iranian deterrent? The answer is plain: the rogue states that rampage in the region and do not want to tolerate any impediment to their reliance on aggression and violence. In the lead in this regard are the U.S. and Israel, with Saudi Arabia trying its best to join the club with its invasion of Bahrain (to support the crushing of a reform movement there) and now its murderous assault on Yemen, accelerating a growing humanitarian catastrophe in that country.

For the United States, the characterization is familiar. Fifteen years ago, the prominent political analyst Samuel Huntington, professor of the science of government at Harvard, warned in the establishment journal "Foreign Affairs" that for much of the world the U.S. was "becoming the rogue superpower ... the single greatest external threat to their societies." Shortly after, his words were echoed by Robert Jervis, the president of the American Political Science Association: "In the eyes of much of the world, in fact, the prime rogue state today is the United States." As we have seen, global opinion supports this judgment by a substantial margin.

Furthermore, the mantle is worn with pride. That is the clear meaning of the insistence of the political class that the U.S. reserves the right to resort to force if it unilaterally determines that Iran is violating some commitment. This policy is of long standing, especially for liberal Democrats, and by no means restricted to Iran. The Clinton Doctrine, for instance, confirmed that the U.S. was entitled to resort to the "unilateral use of military power" even to ensure "uninhibited access to key markets, energy supplies, and strategic resources," let alone alleged "security" or "humanitarian" concerns. Adherence to various versions of this doctrine has been well confirmed in practice, as need hardly be discussed among people willing to look at the facts of current history.

These are among the critical matters that should be the focus of attention in analyzing the nuclear deal at Vienna, whether it stands or is sabotaged by Congress, as it may well be.

Read all about it here.

And as to the nuclear financial deals abrewing (largely unreported on) again:

They’re Shouting from the Rooftops About Junk Bond Dangers – $2.2 Trillion Too Late

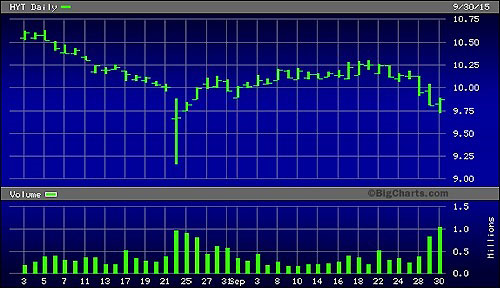

BlackRock Corporate High Yield ETF, August 1 to September 30, 2015

By Pam Martens and Russ Martens

October 1, 2015

An uncanny number of people woke up this week with the same thought – it’s time to panic over the size, structure and illiquidity of the junk bond market. (Not to put too fine a point on it, but "Wall Street On Parade" made the warning in 2013 and again on August 18 of this year.)

On Tuesday morning, it was both Carl Icahn, the famous hostile takeover artist and hedge fund billionaire, along with the more staid academics at the International Monetary Fund (IMF), who issued junk bond warnings. (Junk bonds are corporate debt with ratings below investment grade, also known as “high yield” bonds.)

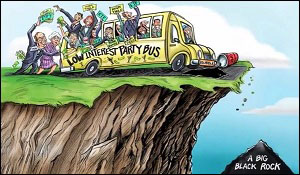

Carl Icahn Blames Janet Yellen and BlackRock for Junk Bond Problems in This Cartoon In His Video

Icahn released a video (see clip below) assigning blame to companies like BlackRock which have bundled illiquid junk bonds into Exchange Traded Funds (ETFs), listed them on the New York Stock Exchange, and sat back and watched as millions of mom and pop investors were sold a bill of goods that these are liquid investments that can be exited at any time during the trading day. The danger, says Icahn, is that liquidity dries up when everyone heads for the exits at the same time. Icahn includes a graph in his video showing that the U.S. junk bond and leveraged loan market has grown from $1 trillion in 2007 to $2.2 trillion today.

Icahn pulled no punches in his assignment of blame, showing a cartoon of Fed Chair Janet Yellen and BlackRock CEO Larry Fink pushing a party bus filled with high yield revelers off a cliff, headed for impact against a “big black rock.” Icahn blames Yellen for keeping rates so excruciatingly low for so long that it created this imprudent search for yield without an appropriate assessment of risk.

The IMF also came out on Tuesday with a warning on junk bonds that carried a brain stumper title: “Market Liquidity Not in Decline But Prone to Evaporate.” Check out the plunge line on August 24 in the above chart for one of BlackRock’s junk bond ETFs to grasp the nuance of that title. August 24 is the day the Dow Jones precipitously dropped 1089 points shortly after the open, closing down 588 points on the day.

The IMF report notes the following:

“ ‘In recent years, factors such as investors’ higher risk appetite and low interest rates have been masking growing underlying fragilities in market liquidity,’ said Gaston Gelos, Chief of the Global Financial Stability Analysis Division at the IMF…

“If financial conditions worsen or investors become weary of a particular asset class or financial market, market liquidity can quickly evaporate. Furthermore, swings in market liquidity in one asset class seem to spill over to other asset classes more frequently, and high-yield and emerging market bonds show some signs of deterioration in market liquidity. As spillovers between asset classes increase, it becomes more likely for a liquidity shock in one market to spread to other markets, possibly leading to a shock to the global financial system, as was the case in 2008.”

Also on Tuesday, the "Wall Street Journal" added to the angst with this report:

“As of mid-September, nearly 15.7% of the roughly 1,720 bonds rated below investment grade traded at distressed levels, the biggest share since 2011, according to Standard & Poor’s Ratings Services. Such bonds were trading with yields at least 10 percentage points over comparable U.S. Treasurys. Yields on bonds rise when prices fall.

“Companies with distressed bonds may not be able to refinance or access other forms of capital, said Diane Vazza, an S&P managing director.”

Jesse Colombo, an economics contributor at Forbes, wrote yesterday: “I believe that junk bonds have experienced a speculative bubble in the past several years thanks to record low interest rates and quantitative easing, which pushed investors into these risky assets in order to earn higher returns. I also believe that a terrifying day of reckoning is ahead when the junk bond bubble ultimately pops.”

On top of mushrooming concerns over distressed U.S. corporate debt, there are growing concerns over foreign corporate debt owed to U.S. banks by struggling companies in emerging markets. Christine Lagarde, Managing Director of the IMF, delivered a speech yesterday in Washington, D.C. to the Council of the Americas which delineated the problem. Lagarde stated:

“…many emerging and developing economies responded to the global financial crisis with bold counter-cyclical fiscal and monetary actions. By using these policy buffers, they were able to lead the global economy in its time of need. And over the past five years, they have accounted for almost 80 percent of global growth.

“These policy actions generally went together with an increase in financial leverage in the private sector, and many countries have incurred more debt – a significant portion of which is in U.S dollars.

“So rising U.S. interest rates and a stronger dollar could reveal currency mismatches, leading to corporate defaults – and a vicious cycle between corporates, banks, and sovereigns.”

Lagarde is referring to the fact that the currencies of emerging market countries have declined dramatically against the U.S. dollar as the U.S. Fed has talked up the dollar with persistent predictions that it would be raising interest rates this year. That has caused the amount of the debt owed by emerging market companies to mushroom, since it takes more of their local currency to pay back the debt in U.S. dollars.

This raises another serious question. Would the benefit to U.S. mega banks from a Fed rate hike (allowing them to increase their loan rates) be more than offset by defaults of emerging market debt that resides quietly at present on their books?

"Bloomberg Business" has a story out this morning suggesting that there will not be a rational resolution to this problem. Japan’s $1.2 trillion government pension fund has announced it plans to invest in junk bonds.

Is Stock Investing for Suckers?

By Pam Martens and Russ Martens

September 30, 2015

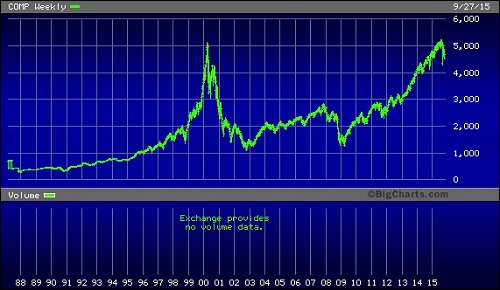

Nasdaq Index Chart Since 1988

On March 10, 2000 the Nasdaq stock market, which is supposed to hold the technology and startup companies that will keep America globally competitive in the future, closed at a high of 5,048.62. Yesterday, more than 15 years later, it closed at 4,517.32, a decline of 10.5 percent from its level of March 2000.

To fully grasp the unprecedented nature of the Nasdaq bubble of 2000, one has to look at where the three big stocks are today that made that 5,000 mark possible 15 years ago. Just three stocks, Microsoft, Cisco, and Intel, were valued at a market cap of $1.89 trillion in 2000. As of yesterday’s close, those three stocks had a combined market cap of $616.137 billion – a shrinkage of 67 percent after more than 15 years.

Much of the hype, as well as the money, that surrounded Microsoft, Cisco and Intel in early 2000, has moved to Apple today, which also trades on the Nasdaq. As of yesterday’s close, Apple commands a market value of $621.9 billion.

Back on March 19, 2000 the Silicon Valley Business Journal reported that one analyst was predicting Cisco was headed toward a market cap of $1 trillion. (Its market cap at yesterday’s close was $129.7 billion, down 80 percent from 2000.)

The article noted that “Thirty-seven investment banks recommend either a ‘buy’ or a ‘strong buy.’ None recommend a ‘sell’ or even a ‘hold.’ ”

On March 23 of this year, an analyst at Cantor Fitzgerald made the same frothy market prediction that Apple would hit a $1 trillion market cap. It’s lost $122 billion in market cap since that call.

The Federal government has two decades of evidence that the integrity of Nasdaq as a stock market has been repeatedly compromised. Yet it does nothing material to rein in the abuses.

The excesses leading up to the crash of 2000-2002 and the crash of 2008-2009 resulted from a highly orchestrated wealth transfer machine on Wall Street that was allowed to operate with impunity from the Federal regulators. As we reported in 2008:

[Regarding the Nasdaq boom of the late 90s] “First, Wall Street firms issued knowingly false research reports to trumpet the growth prospects for the company and stock price; second, they lined up big institutional clients who were instructed how and when to buy at escalating prices to make the stock price skyrocket (laddering); third, the firms instructed the hundreds of thousands of stockbrokers serving the mom-and-pop market to advise their clients to sit still as the stock price flew to the moon or else the broker would have his commissions taken away (penalty bid).

While the little folks’ money served as a prop under prices, the wealthy elite on Wall Street and corporate insiders were allowed to sell at the top of the market (pump-and-dump wealth transfer).

“Why did people buy into this mania for brand-new, untested companies when there is a basic caveat that most people in this country know, i.e., the majority of all new businesses fail? Common sense failed and mania prevailed because of massive hype pumped by big media, big public relations, and shielded from regulation by big law firms, all eager to collect their share of Wall Street’s rigged cash cow.

[Regarding the 2008 market]“The current housing bubble bust is just a freshly minted version of Wall Street’s real estate limited partnership frauds of the ‘80s, but on a grander scale. In the 1980s version, the firms packaged real estate into limited partnerships and peddled it as secure investments to moms and pops.

The major underpinning of this wealth transfer mechanism was that regulators turned a blind eye to the fact that the investments were listed at the original face amount on the clients’ brokerage statements long after they had lost most of their value.

“Today’s real estate related securities (CDOs and SIVs) that are blowing up around the globe are simply the above scheme with more billable hours for corporate law firms.

“Wall Street created an artificial demand for housing (a bubble) by soliciting high interest rate mortgages (subprime) because they could be bundled and quickly resold for big fees to yield-hungry hedge funds and institutions. A major underpinning of this scheme was that Wall Street secured an artificial rating of AAA from rating agencies that were paid by Wall Street to provide the rating. When demand from institutions was saturated, Wall Street kept the scheme going by hiding the debt off its balance sheets and stuffed this long-term product into mom-and-pop money markets, notwithstanding that money markets are required by law to hold only short-term investments.

To further perpetuate the bubble as long as possible, Wall Street prevented pricing transparency by keeping the trading off regulated exchanges and used unregulated over-the-counter contracts instead. (All of this required lots of lobbyist hours in Washington.)”

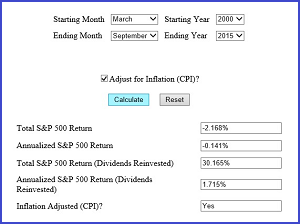

S&P Returns, March 2000 to Present With Dividends Reinvested and Adjusted for Inflation

You are likely thinking that Nasdaq doesn’t reflect the performance of the broader market. You will likely be shocked to see the performance of the Standard and Poor’s 500 index of stocks starting from March 2000 to September 2015, courtesy of this handy online calculator. Even with dividends reinvested, the S&P has delivered a paltry 1.715 percent annualized return since March 2000 on an inflation adjusted basis. And that’s before paying taxes on dividends.

Even if you are invested in diversified, actively managed stock mutual funds, over a working lifetime you are likely to lose two-thirds of your money because of the management fees, according to a "PBS Frontline" report.

This would also be a good time to remember that stock market performance following epic financial crashes that ravage the economy can be hazardous to your wealth. Following the 1929 crash, the stock market did not set a new high until 1954 – 25 years later.

Yesterday, the Securities and Exchange Commission announced that it will hold a hearing on October 27, open to the public, on the stock market’s structure. The SEC has had 15 years since the revelations of the rigged market of 2000 and 7 years since the worst market collapse since the Great Depression to actively engage in reining in the abuses. Yesterday’s announcement was decidedly too little too late.

As Glencore Is Compared to the Fall of Lehman, It Shows Up in Kids’ 529 College Plans

Check your long-term investments NOW.

The Pentagon’s Brain

In her last work, Annie Jacobsen gave us a look at Area 51. Now she talks to "WhoWhatWhy"’s Jeff Schechtman about the trove of government secrets connected to DARPA, the Defense Advanced Research Project Agency. That’s the secret military R&D labs that gave us the Internet, Agent Orange, drones, and advanced research into human cloning.

Trump vs. Fiorina

At CNN’s Republican debate, and ever since, Donald Trump and Carly Fiorina have been attacking each other’s business records — which is sort of like a fight between asbestos and thalidomide.

I admit it's hard to know whom to pull for to go down first.

No comments:

Post a Comment