I'd say those executive bonuses were well worth it, god, er . . . Lloyd.

*Having a steady pool of billions of dollars to prop up a stock’s share price might seem like a neat trick to top corporate executives whose compensation is tied, in part, to the performance of the company’s stock, but it does little to help a nation struggling from the aftermath of the economic ravages unleashed by the big bank financial crash in 2008.

U.S. GDP was negative at -2.9 percent in this year’s first quarter. The U.S. Bureau of Labor Statistics shows a current labor force participation rate of just 62.8 percent, the lowest rate since the late 1970s and owing in part to discouraged workers who have given up on looking for a job. Surely using capital to grow a business and create good jobs should trump retiring stock.

. . . In JPMorgan’s London Whale episode, the firm taught us why Wall Street trading houses were so engaged for decades in lobbying to repeal the Glass-Steagall Act. JPMorgan had used hundreds of billions of dollars of its Chase bank depositors’ funds to make high-risk bets in derivatives in London. It lost those bets to the tune of $6.2 billion. In the years when JPMorgan had won those bets with depositor funds, it kept the profits for the house and richly rewarded its executives with outsized compensation and bonuses. Simply stated, the repeal of Glass-Steagall allowed the use of other people’s money to enshrine heads-we-win/tails-you-lose on Wall Street.

I just love it when old-time stories about really bad guys are made new again (because they never went away?) or at least updated with all the new tawdriness on display. Seems that everything old is new again (or never was allowed to get that old). (Get your cheapo Econ. degree here today, friends!)

I should only run a part of this fabulous bit of journo hell, but can't resist it for my faithful readers who hate to click around too much. Hat tip to Heather P (Digby), who is always on the case and is now published regularly to our delight by Salon!

If there’s one thing Republicans have learned over the years it’s to never let legalities stand in the way of a good fundraising scam. And one of their best cons ever was Jack Abramoff and Ralph Reed’s brilliant scheme to con millions from Indian tribes to run a supposedly religious-based anti-gambling campaign against the tribes’ rivals in order to gain exclusive gambling rights. And even better was the revelation that they were ripping off their own Christian clients as well. What’s not to like? Publicly appeasing religious conservatives at the expense of Indian tribes on behalf of other Indian tribes for whom they have nothing but contempt? It’s beautiful. Only Iran-Contra comes to mind as a similarly elegant illegal scheme.

Unfortunately for them, the whole thing unraveled when other illegal behaviors involving Abramoff and his cohorts were revealed as part of an ongoing corruption probe by the Department of Justice. The revelation of the emails involving a Mississippi Indian tribe were particularly ugly.

Abramoff and his cronies referred to the tribes as “troglodytes,” “monkeys,” “morons” and “f’ing idiots” and laughed at the rubes who were paying them tens of millions of dollars to deliver basically nothing of value. As you would imagine, the tribes were not amused.

The religious right groups were defrauded in a different way, by being led to believe that good Christian gentlemen like Abramoff’s buddy Ralph Reed really shared their belief that gambling is a sin only to find out that his activities were actually helping to promote it. (Elmer Gantry was written all the way back in 1927, so it’s not as if this con-man theme is anything new in such circles.) Still, it had to be a disappointment to see one of their young, evangelical stars tarnished with such crude pecuniary corruption.

The triumvirate of Jack Abramoff, Ralph Reed and Grover Norquist went all the way back to the early ’80s when they were young Republican Revolutionaries. Each in their own way represented one of the big tent poles of the modern conservative movement: Reed was the religious right, Norquist was the no tax pledge, and Abramoff was the big money lobbyist.

They were a juggernaut during the Gingrich and Bush eras, pulling together a coalition of small government conservative Christians and wielding tremendous influence in the Republican Party and on Capitol Hill.

Norquist managed to keep his hands fairly clean and escaped the denouement, but in the end, Abramoff pleaded guilty to a number of crimes and went to jail as did some others implicated in the schemes. Several politicians lost their seats. Ralph Reed was chastised by the voters of Georgia when he later ran for lieutenant governor and lost decisively.

So, one might think that as unseemly as the whole episode was, in the end the system worked.

But it didn’t.

Yesterday, Politico revealed that the latest GOP group of power brokers, the Republican State Leadership Committee, best known for its hugely successful campaigns around the country to turn statehouses into GOP majorities in order to redraw the congressional maps in their favor, has been running similar schemes as recently as 2010 in the state of Alabama. They reported:

At the height of its political emergence, the RSLC was implicated in a risky campaign finance scheme that an internal report warned could trigger “possible criminal penalties” and “ultimately threaten the organization’s continued existence,” according to a confidential document Politico obtained from a source.They understood that the Mississippi conservatives don’t approve of Indian tribes and their filthy gambling:

Never disclosed until now, the document detailed an investigation into alleged misconduct by multiple RSLC officials during the crucial 2010 election cycle: It charged that national RSLC leaders conspired improperly with the leader of the Alabama Republican Party to use the RSLC as a pass-through for controversial Indian tribe donations, essentially laundering “toxic” money from the gaming industry by routing it out of state and then back into Alabama.

It is … common knowledge and wisdom in Alabama that taking a contribution directly from the tribe is political suicide for a Republican candidate or public official,” the report stated. “Here RSLC appears to have served as both a recipient of the funds in question and as a donor of the funds back to Alabama, thereby permitting Mike Hubbard to do indirectly that which he could not do directly.”They even used some of Abramoff’s old money-laundering services:

It also sent $100,000 to a group, Citizens for a Better Alabama, that the report describes as “the renamed ‘Citizens Against Legalized Lottery’ (‘CALL’), one of the Christian groups through which Jack Abramoff funneled Choctaw Indian-money.”The RSLC reports that the people responsible are no longer with the committee and those who were kicked out say there wasn’t anything illegal about what they were doing anyway, all of which might be true. At the heart of this matter is more of the Southern gothic Mississippi politics we’ve been observing ever since the McDaniel-Cochran primary — a Republican Party in the midst of a ruthless family quarrel. This story indicates that the dimensions of that argument are more complicated than was previously known. It’s falling apart at the seams.

Today Jack Abramoff, himself a highly religious man, is making much of his rehabilitation and decries his formerly corrupt ways. He also does interviews with the right-wing site World Net Daily and calls Elizabeth Warren and Hillary Clinton bolsheviks who are allegedly “taking over” everything. Ralph Reed has made another comeback with his new religious right group the “Faith and Freedom Coalition” and is back in the warm embrace of the GOP establishment and the Christian right. Grover Norquist continues to be the influential keeper of the no-tax pledge.

And Republicans are still ripping off Indian tribes and Christian conservatives like there’s no tomorrow. This is the system and they know how to work it. If it ain’t broke, why fix it?

I may be a few days late with the next few newsy items, but speaking of old schemes being "made new" again . . . has anyone actually studied what happened before the crash of 1929? Or even 2008?

These are not new ideas, folks! (Love to use that "folks" designation when we're being serious, don't we?)

Senate Bombshell Testimony Today: Citigroup and Bank of America Stock Worthless Without Implied Government Guarantees

By Pam Martens: July 31, 2014

Senator Sherrod Brown, Chairman of the Senate Banking Subcommittee on Financial Institutions and Consumer Protection, will take testimony at 2 p.m. today on market subsidies enjoyed by implied future government bailouts of the too-big-to-fail status of Wall Street’s bloated and serially malfeasant banks. The hearing is set to coincide with a new report from the Government Accountability Office (GAO).

An early peek at written testimony by three separate professors set to testify guarantees a belated July 4 fireworks display — one that is not likely to enjoy a welcome reception within the Wall Street corridors of power. Expect the phone lines of lobbyists and congressional campaign managers to be lighting up all over the nation’s capitol this afternoon.

Professor Edward J. Kane

Edward J. Kane, Professor of Finance at Boston College will get things off to a rousing start by telling the Subcommittee that any suggestion that the Dodd-Frank financial reform legislation ended the implied government guarantees “is a dangerous pipe dream.”

A powerful argument made by Kane (see full text of testimony linked below) is that these too-big-to-fail banks enjoy not just a market subsidy on their debt but on their equity as well. Kane writes:

“Being TBTF [too-big-to-fail] lowers both the cost of debt and the cost of equity. This is because TBTF guarantees lower the risk that flows through to the holders of both kinds of contracts. The lower discount rate on TBTF equity means that, period by period, a TBTF institution’s incremental reduction in interest payments on outstanding bonds, deposits, and repos is only part of the subsidy its stockholders enjoy.

The other part is the increase in its stock price that comes from having investors discount all of the firm’s current and future cash flows at an artificially low risk-adjusted cost of equity. This intangible benefit generates capital gains for stockholders and shows up in the ratio of TBTF firms’ stock price to book value. Other things equal (including the threat of closure), a TBTF firm’s price-to-book ratio increases with firm size…”

Kane then lands this bombshell: “The warranted rate of return on the stock of deeply undercapitalized firms like Citi and B of A [Bank of America] would have been sky high and their stock would have been declared worthless long ago if market participants were not convinced that authorities are afraid to force them to resolve their weaknesses.”

Kane goes on to say that it is “shameful” for government officials to suggest that bank bailouts were good deals for taxpayers. Kane writes: “On balance, the bailouts transferred wealth and economic opportunity from ordinary taxpayers to much higher-income stakeholders in TBTF firms. Ordinary citizens understand that this is unfair and officials that deny the unfairness undermine confidence in the integrity of economic policymaking going forward.”

Professor Anat Admati

Anat Admati, Professor of Finance and Economics at the Graduate School of Business at Stanford University, who was voted one of Time Magazine’s top 100 influential people in April of this year, writes in her testimony that “The Fed has the responsibility and the ability to protect the public, yet as a regulator, it has failed the public.”

Admati’s testimony places the blame of the 2007-2009 Wall Street collapse squarely at the feet of regulators, writing in her testimony:

“Financial crises are sometimes portrayed as if they were unpreventable natural disasters, implying that bailouts are similar to emergency aid after an earthquake. This narrative is misleading. The crisis of 2007-2009 was an implosion of a system that had become too fragile, reckless, and distorted. Regulatory failures, including flawed and ineffectively enforced regulations, must take much of the blame for the excessive fragility and the buildup of risk.”

Admati says today’s banking system “is disturbingly similar to allowing heavy trucks with dangerous cargo to drive recklessly at 95 miles per hour in residential neighborhoods. If drivers get a bonus for reaching the destination quickly, and face little risk of injury or death even in an explosion (imagine that they have a special protective mechanism), they will drive recklessly and endanger innocent citizens…”

Admati writes further:

“Encouraging and subsidizing banks to fund themselves with as much debt as is currently allowed (up to 95% for the large bank holding companies) is as perverse as encouraging and subsidizing reckless speed for trucks or rewarding the captains of large oil tankers to go ever closer to the coast. More equity would force banks to stand more on their own when they take risk, rather than shift some of the risk and cost of bearing it to others. Shareholders who benefit from the upside, and not creditors or taxpayers, should be the ones to bear the downside.”

Deniz Anginer, Assistant Professor at the Pamplin Business School at Virginia Tech, also gives Dodd-Frank a thumbs down in terms of ending too-big-to-fail, writing:

“…we find that Dodd-Frank did not significantly alter investors’ expectations that the government will bail out TBTF financial institutions should they falter. Despite its no-bailout pledge, Dodd-Frank leaves open many avenues for future TBTF rescues. For instance, the Federal Reserve can offer a broad-based lending facility to a group of financial institutions in order to provide a disguised bailout to the industry or a single firm…”

The full list of witnesses set for the hearing appears below.

Mr. Lawrance L. Evans [view testimony]

Director, Financial Markets and Community Investment

U.S. Government Accountability Office

Dr. Deniz Anginer [view testimony]

Assistant Professor of Finance

Pamplin School of Business, Virginia Tech

Dr. Edward Kane [view testimony]

Professor of Finance

Boston College

Dr. Anat Admati [view testimony]

George G.C. Parker Professor of Finance and Economics

Graduate School of Business, Stanford University

Mr. Douglas Holtz-Eakin [view testimony]

President

American Action Forum

Buying back your own stock sounds like a confidence-inspiring executive move, doesn't it?

Not so much now actually.

JPMorgan Has Spent $18 Billion Buying Back Its Own Stock in Four Years

By Pam Martens and Russ Martens

July 30, 2014

As Wall Street On Parade reported last week, Jeffrey Kleintop, Chief Market Strategist for LPL Financial, reports that corporations are now the single largest buying source for U.S. stocks – authorizing buybacks of their own stocks to the tune of $754.8 billion in 2013 alone.

And it’s a long-term trend. According to Birinyi Associates, for calendar years 2006 through 2013, corporations authorized $4.14 trillion in buybacks of their own publicly traded stock in the U.S. — raising the question, just what kind of a bull market is this?

JPMorgan Chase, the largest U.S. bank by assets, has turned share buybacks into an art form, buying back a whopping $17,945,000,000 of shares from 2010 through 2013. In just the calendar year of 2011, JPMorgan spent a stunning $8,827,000,000 on stock buybacks.

According to JPMorgan’s most recent quarterly report filed with the Securities and Exchange Commission, “the Firm’s Board of Directors has authorized the Firm to repurchase $6.5 billion of common equity between April 1, 2014, and March 31, 2015.”

If the full authorization of $6.5 billion is spent by the first quarter of next year, JPMorgan will have tapped its capital to the tune of $24.5 billion – not to lend to deserving businesses or home buyers or consumers, but to binge on its own stock buybacks.

*Having a steady pool of billions of dollars to prop up a stock’s share price might seem like a neat trick to top corporate executives whose compensation is tied, in part, to the performance of the company’s stock, but it does little to help a nation struggling from the aftermath of the economic ravages unleashed by the big bank financial crash in 2008.

U.S. GDP was negative at -2.9 percent in this year’s first quarter. The U.S. Bureau of Labor Statistics shows a current labor force participation rate of just 62.8 percent, the lowest rate since the late 1970s and owing in part to discouraged workers who have given up on looking for a job. Surely using capital to grow a business and create good jobs should trump retiring stock.

There are other reasons to worry about this binge in stock buybacks. First, many corporations are borrowing heavily to fund these buybacks. There is also a concern that the public is given very little information about how these buybacks are conducted and by whom.

That concern has grown exponentially as dark pool trading data has started being released, for the first time ever, by the Financial Industry Regulatory Authority (FINRA), Wall Street’s self-regulator. (A dark pool is an unregulated stock exchange which does not make bids and offers on stocks transparent to the marketplace; a venue ripe for manipulation.)

FINRA data shows that, week after week, Wall Street’s biggest banks are trading each other’s stocks in their own dark pools and, more inexplicable, the banks are being allowed to trade their own corporate parent’s stock in their own dark pools. How this is compatible with the anti-manipulation statutes of the Securities Exchange Act of 1934 has yet to be explained.

During the week of July 7 to July 11, 2014, 65.8 million shares of JPMorgan Chase traded in total on all venues, including public exchanges like the New York Stock Exchange as well as dark pools. Of that total, according to FINRA data, 11.8 million shares in the same week traded in dark pools or 17.9 percent of all JPMorgan stock traded.

Of the 11.8 million JPMorgan shares which traded in all dark pools for the week of July 7 to July 11, JPMorgan’s own dark pool, JPM-X, traded 1,018,943 shares or 8.6 percent of the total.

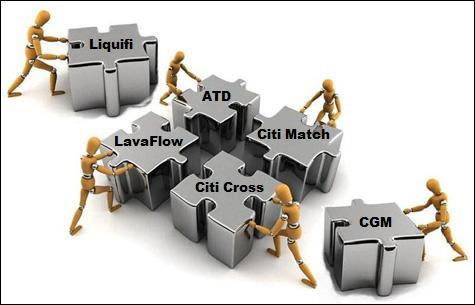

Other global banks that are trading JPMorgan’s stock in their own dark pools, week after week, include UBS; Credit Suisse; Citigroup’s LavaFlow, CitiCross and Liquifi; Deutsche Bank; Goldman Sachs; Bank of America’s Merrill Lynch and Barclays.

Barclays has been charged by the New York State Attorney General, Eric Schneiderman, with lying to its customers about the role of high frequency traders in its dark pool. Barclays has asked to have the charges dismissed on the basis that Schneiderman overreached his authority. UBS announced this week that it is cooperating with a probe into its dark pool.

The accelerated pace of investigations into a long simmering pool of hubris has been stepped up since Michael Lewis launched his book, Flash Boys, with a pronouncement on 60 Minutes on March 30 that the stock market is rigged by high frequency traders and global banks.

Shortly thereafter, the FBI announced that an investigation was already in the works, the New York State Attorney General began issuing subpoenas, and FINRA attempted to look serious with a dark pool action against Goldman Sachs.

The most unsettling aspect of all of this is that the dark pool framework relies on the theory that global investment banks can be trusted to run unregulated stock exchanges, swapping millions of shares of each other’s stocks with no oversight and no transparency. But there is zero basis for that trust.

These are the same banks being charged, month after month, year after year, with cavalierly engaging in collusion with each other to rig market benchmarks for their own self enrichment and to the extreme detriment of market integrity, small investors and the economy at large.

There are only two ways to look at this: Congress and regulators are preposterously naïve about the level of corruption on Wall Street – or they’re part of the conspiracy.

Either way, to restore the public confidence that has permanently left our markets, we need a credible, non conflicted, independent counsel to take charge of the investigations.

FINRA Data Showing Dark Pool Trading in Stock of JPMorgan Chase for Week of July 7, 2014 (Only Top Eight Dark Pools That Traded in the Stock Shown Here)

And we've mentioned all the subsequent shenanigans arising from the vast dark pools before, but did you know that they weren't dark for everyone? As if you didn't.

And how hard is it to say the words "Robert Rubin?"

A cautionary tale about the perils of education if ever there were one.

And "Obama's team?"

Wall Street Journal Reporter: “The Entire United States Market Has Become One Vast Dark Pool”

By Pam Martens and Russ Martens

July 29, 2014

In 2012, Wall Street Journal reporter, Scott Patterson, released his 354-page prescient overview of U.S. market structure titled, Dark Pools: High Speed Traders, A.I. Bandits, and the Threat to the Global Financial System. (For those whose computer prowess is limited to turning on a laptop, like millions of fellow Americans, “A.I.” means artificial intelligence – machines teaching themselves to think like humans, but faster.)

Citigroup, the Bank the U.S. Taxpayer Saved From Insolvency in 2008, Is Operating a Dizzying Array of Dark Trading Pools Today

Patterson comes to an epiphany on page 339 of his book, writing in the notes section: “The title of this book doesn’t entirely refer to what is technically known in the financial industry as a ‘dark pool.’ Narrowly defined, dark pool refers to a trading venue that masks buy and sell orders from the public market. Rather, I argue in this book that the entire United States stock market has become one vast dark pool. Orders are hidden in every part of the market. And the complex algorithm AI-based trading systems that control the ebb and flow of the market are cloaked in secrecy. Investors – and our esteemed regulators – are entirely in the dark because the market is dark.”

We totally agree with Patterson that U.S. markets are the darkest they have ever been in history – from their early origins in the bright sunlight under the Buttonwood tree at 68 Wall to today’s secretive, unregulated stock exchanges known as dark pools that trade in private across America – the lights have gone out. And as each light has flickered and dimmed, public confidence has drained from the system, leaving it today as the unsafe battlefield of hedge funds, high frequency traders and dark pool operators.

Wall Street and its sycophants began this journey into darkness with their push to run their own private justice system on Wall Street in the 1980s.

Called mandatory arbitration, Wall Street was given a green light by the U.S. Supreme Court in its 1987 decision, Shearson/American Express v. McMahon. Since then, cases filed by both customers and employees against Wall Street firms, which could shed critical light and serve as an early warning system on patterns of fraud and abuses, have been removed from the sunlight of open courtrooms into the dark shadows of a private justice system that claimants believe is rigged against them.

Once able to function as its own judge and jury in a justice system designed by its own Wall Street lawyers, the industry was effectively able to keep many of its crimes shielded from the press for years – until they collapsed in massive losses and brought subpoenas.

After its coddlers gave Wall Street its own court system, removed from the prying eyes of the nation’s justice system and the press, Wall Street was ready to begin repealing every other layer of investor protection that had been enacted after Wall Street’s wholesale looting of the country in the late 20s and early 30s.

The most dangerous repeal, of course, was the repeal of the Glass-Steagall Act which had barred Wall Street firms that gambled in stocks from owning insured deposit banks.

Today, the largest trading houses on Wall Street are under the same corporate umbrella as the nation’s largest banks: JPMorgan owns Chase bank; Citigroup owns Citibank; Bank of America owns Merrill Lynch.

In JPMorgan’s London Whale episode, the firm taught us why Wall Street trading houses were so engaged for decades in lobbying to repeal the Glass-Steagall Act. JPMorgan had used hundreds of billions of dollars of its Chase bank depositors’ funds to make high-risk bets in derivatives in London.

It lost those bets to the tune of $6.2 billion. In the years when JPMorgan had won those bets with depositor funds, it kept the profits for the house and richly rewarded its executives with outsized compensation and bonuses. Simply stated, the repeal of Glass-Steagall allowed the use of other people’s money to enshrine heads-we-win/tails-you-lose on Wall Street.

That brings us to today’s dark pools functioning as unregulated stock exchanges which JPMorgan, Citigroup, and Bank of America are also allowed to own and operate along with more than three dozen other firms.

Last week, the SEC brought and settled a case against one of Citigroup’s dark pools, LavaFlow, for the improper use of customer information. One sentence of the SEC’s order was a real shocker. The SEC wrote:

“As of December 31, 2013, the LavaFlow ECN was the largest ECN and the largest ATS as measured by dollar volume executed with over $361 billion in total dollar volume of executions for the fourth quarter of 2013.”

ATS stands for Alternative Trading System, synonymous with dark pool most of the time. Few people on Wall Street know that Citigroup is operating the largest dark pool. As recently as July 22, Bloomberg News reported that Credit Suisse “operates Wall Street’s largest dark pool.”

Wall Street On Parade spent weeks digging through government filings to compile this frightening look into Citigroup’s dark pools and the sea of darkness that has swallowed what was once the pride of a nation – U.S. markets.

Citigroup – the bank that was propped up after its crash in 2008 with $45 billion of TARP funds, over $300 billion in asset guarantees and more than $2 trillion in low-cost loans from the New York Fed, is now effectively an unregulated stock exchange operating in the dark and annualizing at over $1 trillion in dollar volume in stock transactions.

Simultaneously, it is operating insured deposits banks spread across America – all at a time when it has flunked its stress test with the Federal Reserve, which doesn’t have confidence in it to manage its affairs in a sharp downturn.

Citigroup’s previous dark operations – hiding tens of billions of dollars of debt off its balance sheet – contributed to the bank’s collapse in 2008 and its stock losing 60 percent of its value in just the week of November 17-21, 2008. Its regulators were too busy schmoozing with it to see the disaster that was about to befall the bank and the nation.

Under the current market and regulatory structure and lack of meaningful, transparent probes by the U.S. Department of Justice, the public has a very solid basis for distrusting Wall Street.

Wash sales being a crime endangering Wall Street profits . . . ?

Well, let's fix that.

They're no longer a crime.

Wall Street’s Regulators Sell Out on Illegal Wash Sales

By Pam Martens and Russ Martens

July 28, 2014

Bart Chilton, Former CFTC Commissioner, Speaks Out on “Voluminous” Amount of Wash Sales, March 18, 2013

Wash sales – one of the most virulent forms of stock manipulation that bankrupted banks and corporate conglomerates in the Great Depression and intensified the stock market crash of 1929 to 1932 – has reached scandalous proportions in today’s markets. The response from regulators? Gut the rules that make it a crime.

On March 18 of last year, Bart Chilton, then a Commissioner at the Commodity Futures Trading Commission (CFTC), stunned CNBC viewers with the announcement that wash sales were rampant in the futures markets. Speaking to Squawk Box host, Joe Kernen, Chilton stated:

“Well these wash sales, Joe, people know they’re illegal; they’re not allowed. A wash sale is when somebody trades with themselves. But what we’ve discovered is that they are going on at this large, voluminous level. I mean, to me, a shocking level. And they’re impacting what people see as volume. So this is an area that we’re going to review to ensure that markets are operating efficiently and effectively. Who knows what sort of impact they’re having. And it raises a host of policy questions that we have out there, because this stuff just shouldn’t be allowed.”

Volume is hardly the only problem with wash sales: the age old tactic of a wash sale is to pump a stock’s price so insiders can bail out at the top and transfer the losses of a worthless or inflated security to uninformed investors. This is done by the same party conducting or authorizing simultaneous buying and selling in the stock, typically making sure trades occur at ever rising prices until the operators have unloaded their stock. Without that support, the price crashes.

Laws making it illegal for one party to be on both the buy and sell sides of a stock transaction were implemented during the legislative reforms of Wall Street in the 1930s.

They have had legal certainty for the past 80 years until this May 1 when Wall Street’s coddling, captured regulators, the Securities and Exchange Commission and the Financial Industry Regulatory Authority (FINRA), gutted the wash sale rules beyond recognition – even changing the name of the illegal practice from “wash sale” to the benign “self trade.”

The CME Group, which runs the Chicago Mercantile Exchange, the largest futures market in the world, similarly gutted its rule language in June of last year, writing:

“The Advisory Notice clarifies that orders entered by different traders making fully independent trading decisions that unintentionally and coincidentally match opposite each other on the electronic platform will not be deemed a wash trade provided that the orders are entered in good faith for the purpose of executing bona fide transactions, are not prearranged and that each trader enters their order without knowledge of the other trader’s order.” (This while regulators on multiple continents are charging cartels of traders with rigging everything from Libor to metals to currency markets and chat room transcripts show the casualness with which traders rig with abandon.)

With the gutting of the clear intention of the law, today a Citigroup stock trading operation could be on both the buy and sell side of a trade just as long as the buy happens on one trading desk and the sell happens on a different trading desk within Citigroup. This would render the transaction “bona fide” under this perverted logic – which makes the leap that computer algorithms on separate trading desks can’t be programmed to rig markets with wash sales.

This is an excerpt from the SEC’s approval of the gutted rule submitted by FINRA:

“The proposed rule change requires FINRA members to have policies and procedures in place that are reasonably designed to review their trading activity for, and prevent, a pattern or practice of self-trades resulting from orders originating from a single algorithm or trading desk, or from related algorithms or trading desks. Additionally, the proposed rule change states that transactions resulting from orders that originate from unrelated algorithms or from separate and distinct trading strategies within the same firm would generally be considered bona fide self-trades.”

Following the 1929 stock market crash, which over the next 30 months erased 90 percent of the stock market’s value, the U.S. Senate Committee on Banking and Currency launched an exhaustive investigation into the manipulative devices and looting operations of Wall Street’s biggest names. The Committee was smart enough then to realize that it would have to exhaustively examine the structure of the market, not just the conduct of individual actors, to understand how an institutionalized wealth transfer system had been carried out. The tactic of wash sales to rig stock prices was repeatedly uncovered by the Senate investigation. One of the biggest cases on which the Committee spent days was the Samuel Insull wash sales.

In 1934 the Associated Press introduced to the American public the financial nightmare that can ensue from wash sales. Samuel Insull had built an electric utility conglomerate using a holding company structure that disguised mushrooming debts. Insull kept the scheme going by artificially inflating the conglomerate’s publicly traded stock through more than a million wash sales.

On October 20, 1934, The Associated Press explained the “wash sale” allegations against Insull: “Prosecutors closed the third week of their case against Samuel Insull, Sr. today with testimony that ‘wash sales’ helped make the ‘jewels of the Insull empire’ sparkle for investors.”

The next day, on October 21, 1934, the Milwaukee Journal reported that through his own investment company, the Corporation Securities Company, prosecutors charged Insull with conducting 1,049,624 trades in his own stock out of total market trades of 1,695,450 that occurred from April 30, 1930 to January 12, 1932. When the Insull house of cards collapsed in 1932, investors in its stocks and bonds across America were wiped out, losing hundreds of millions of dollars.

Insull fled to Europe to beat an indictment but was eventually captured and returned by authorities. Despite overwhelming evidence of payoffs and market rigging, Insull was acquitted at trial.

The 1930s Senate investigation was initiated less than three years after the 1929 crash. The 2008 crash occurred six years ago and yet, today, no such intense investigation of market structure has been undertaken by Congress.

What we have seen instead are isolated hearings, most of which are devoid of oath-taking or subpoenas. Only a small handful of Senators even care enough to show up for the Senate Banking hearings. (The Senate Permanent Subcommittee on Investigations, of course, has done a herculean job in its Wall Street investigations but its plate is simply too full. The Senate Banking Committee has failed to pull its weight.)

Eighty years of sound, prudent securities law has now been wiped out as Congress seems to muddle about in a daze. The pool operators of the 1930s have been reincarnated today in the form of Wall Street’s dark pools.

The protections of the depression-era Glass-Steagall Act which barred the Wall Street speculators from getting ownership of insured deposit banks to gamble in stocks and derivatives – wiped away with the passage of the Gramm-Leach-Bliley Act in 1999. Now rampant wash sales have been given a less onerous name and a green light by the top securities cop – a cop that today is staffed with Wall Street’s favorite former lawyers.

Wall Street’s technology gurus can create artificial intelligence programs that can trade in microseconds. Wall Street certainly has the capability of creating wash blockers that would prevent all wash trades from occurring. The coddling regulators had no need to gut the rules other than to once again show their fealty to their pals on Wall Street.

And one more for the road.

Don't drink and drive.

Lawsuit Stunner: Half of Futures Trades in Chicago Are Illegal Wash Trades

By Pam Martens: July 24, 2014

Terrence Duffy of the CME Group Testifying Before the Senate on May 13, 2014

Since March 30 of this year when bestselling author, Michael Lewis, appeared on 60 Minutes to explain the findings of his latest book, Flash Boys, as “stock market’s rigged,” America has been learning some very uncomfortable truths about the tilted playing field against the public stock investor.

Throughout this time, no one has been more adamant than Terrence (Terry) Duffy, the Executive Chairman and President of the CME Group, which operates the largest futures exchange in the world in Chicago, that the charges made by Lewis about the stock market have nothing to do with his market. The futures markets are pristine, according to testimony Duffy gave before the U.S. Senate Agriculture Committee on May 13.

On Tuesday of this week, Duffy’s credibility and the honesty of the futures exchanges he runs came into serious question when lawyers for three traders filed a Second Amended Complaint in Federal Court against Duffy, the Chicago Mercantile Exchange, the Chicago Board of Trade and other individuals involved in leadership roles at the CME Group.

The conduct alleged in the lawsuit, backed by very specific examples, reads more like an organized crime rap sheet than the conduct of what is thought by the public to be a highly regulated futures exchange in the U.S.

The lawyers for the traders begin, correctly, by informing the court of the “vital public function” that is supposed to be played by these exchanges in “providing price discovery and risk transfer.” They then methodically show how that public purpose has been disfigured beyond recognition through secret deals and “clandestine” side agreements made with the knowledge of Duffy and his management team.

The most stunning allegation in the lawsuit is that an estimated 50 percent of all trading on the Chicago Mercantile Exchange is derived from illegal wash trades.

Wash trades were a practice by the Wall Street pool operators that rigged the late 1920s stock market, leading to the great stock market crash from 1929 through 1932 and the Great Depression. Wash trades occur when the same beneficial owner is both the buyer and the seller. Wash trades are banned under United States law because they can falsely suggest volume and price movement.

The lawsuit says Duffy and his management team are tolerating wash trades “because they comprise by some estimates fifty percent of the Exchange Defendants’ total trading volume and also because HFT transactions account for up to thirty percent of the CME Group’s revenue.”

The complaint indicates that the plaintiffs have a “Confidential Witness A,” a high frequency trader, who has given them a statement that wash trades are used by high frequency traders as part of a regular strategy to detect market direction and “to exit adverse trades when the market goes against their positions.”

The strategy works like this, according to the complaint:

“HFTs [high frequency traders] continuously place small bids and offers (called bait) at the back of order queues to gain directional clues. If the bait orders are hit, the algorithm will place follow-up orders to either accumulate favorable positions or exit ‘toxic’ risks, a process which leverages bait orders to gain valuable directional clues as to which way the market will likely move. The initial bait orders are very small while subsequent orders, once market direction has been identified, are very large. A portion of the large orders that follow the smaller bait orders are wash trades.”

Another very serious charge is that some of the defendants in the lawsuit who are in leadership roles in management at the futures exchanges, have “equity interests” in the very high frequency trading firms that are benefitting from these wash trades. The complaint states:

“The Exchange Defendants profit from the occurrence of wash trades and have a vested interest in not having more robust safeguards against them because they contribute significantly to the Exchange Defendants’ volume numbers and revenue. Were the volume of wash trades excluded from the Exchange Defendants’ volume and revenue numbers, the radically reduced volume numbers would exert adverse pressure on the CME Group’s stock price, not to mention the revenue to members of CME Group’s governance who have equity interests in participating HFTs in addition to stock ownership in the CME Group, Inc.”

In addition to wash trades, the lawsuit charges that the CME Group has entered into “clandestine” incentive agreements.

“Defendants have entered into clandestine incentive/rebate agreements in established and heavily traded contract markets with favored firms such as DRW Trading Group and Allston Trading, paying up to $750,000.00 per month in one of the most heavily traded futures contracts in the world. At no time during the Class Period have Defendants voluntarily revealed to the trading public that these material agreements exist in established markets. Defendants through their lawyers have repeatedly ridiculed the suggestion that clandestine agreements exist.”

The complaint identifies another “Confidential Witness B” who has provided information on “the existence of a clandestine rebate agreement between the CME and a very large volume HFT firm that trades in the S&P500 E-Mini contract.” That’s a stunning allegation since the S&P500 E-Mini was thought to be one of the most liquid contracts in the U.S. The complaint correctly notes that “there can be no economically justified reason, such as to develop thinly traded markets, that would justify the CME and CME Group to maintain clandestine incentive agreements in this particular market, other than the improper intent.”

Another trick to get an early peek at trading information is referred to in the complaint as the “Latency Loophole,” which “allows certain market participants to know that orders they entered were executed and at what price, and to enter many subsequent orders, all before the rest of the market participants found out the status of their own initial orders.”

The complaint explains that the ability to continuously enter orders and get trade confirmations “of the price at which these orders are filled, before the rest of the public even knows about the executed trades,” empowers high frequency traders with “a massive informational and time advantage in discerning actual price, market direction and order flow before anyone else.”

By providing just a select group of market participants and high frequency traders with this “sneak peek” advantage, says the complaint, the defendants engaged in a “fraud on the marketplace.”

The Justice Department and FBI have opened investigations into high frequency trading. Let’s hope that includes both stock and futures exchanges.

The traders bringing the lawsuit, which is filed as a class action, are William Charles Braman, Mark Mendelson and John Simms. Lawyers for the plaintiffs are R. Tamara de Silva, who maintains a private practice, and lawyers from O’Rourke & Moody.

The suit was filed in the U.S. District Court for the Northern District of Illinois. The Civil Docket for the case is #: 1:14-cv-02646 and has been assigned to Judge Charles P. Kocoras. The CME Group is represented by the law firm Skadden, Arps, Slate, Meagher & Flom, LLP.

No comments:

Post a Comment