The Keiser Report is the best news reporting you will see of this catastrophic situation anywhere. Today, he interviews, among others, James Kunstler of Clusterfuck! Give it a few moments. You won't regret it!

I've been reading Neil Garfield for quite a long time and I have to tell you that it's addictive. He has one of the best opinion blogs (with the economic data to back it up) that I've seen anywhere detailing what I'm starting to think of as "The Great American Bailout of Financial Liars: Foreclosure? (Fraudclosure!)." Please do yourself a favor and read through this essay of his (notes, actually, on all things financially disturbing) on what has happened up to now legislatively and judicially, and why we may never see the end of this now-obvious fraud that has ravaged millions who may never recover.

Happy Valentines!

MarketWatch 666

“All media exist to invest our lives with artificial perceptions and arbitrary values”

Sunday, February 12, 2012

Notes on the Fraudclosure Bailout, the Dysfunctional Congress, Consumer Credit, et al.

You have likely all heard the depressing news this past week that all the state attorney generals caved in & "agreed in principle" to the administration's $25 billion mortgage fraud settlement with the 5 major banks who are mortgage loan servicers (oklahoma's AG reached a separate settlement worth $18.6 million); since virtually nothing had changed in the terms of this that we knew about a few weeks ago, it's apparent that all the rhetoric about bringing the perpetrators to justice of recent weeks was either orchestrated for public consumption or positioning as a way of negotiating for those state attorneys a bigger piece of the national pie...the lion's share of this deal is a three year $17 billion "commitment" to "homeowner relief" by the 5 servicers, which is expected to be through principal reduction, and since those loans are effectively owned by the holders of the mortgage backed securities those loans are pledged to, it will be the investors in those MBS that take the hit, not the banks; furthermore, since the total underwater equity in the US is estimated at $700 billion, this $17B is less than 3% of the total, and will like only be distributed to one million of the approximately 11 million borrowers who are underwater; loans outstanding that are owned or controlled by fannie & freddie, the majority of the total, will not be participating in this settlement

...The servicers also "commit" an additional $3 billion to refinance underwater homes at 5.25%, a lower mortgage rate than they are now paying...both the principal reduction and the refinancing aspects of this settlement tend to help the banks, because they encourage underwater homeowners to stay current & keep making house payments; as we've seen, over 6 million, or one in eight indebted homeowners, have already stopped paying on their mortgages...there will also be $5 billion in direct payments ($4.25 billion to the states and $750 million to the federal government)...of those funds to the states, about $3 billion will be distributed to whatever portion of the approximately four million homeowners who have already been fraudulently foreclosed on between 2008 and 2011 who apply and are determined to be eligible; this is expected to amount to a payment of between a $1500 and $2000 each for those who've already had their homes taken illegally...the remainder will go to the state attorney generals offices, to defray their expenses in managing this program…to put it in perspective, the total price tag on this settlement of $25 billion is only one tenth the cost of the state's 1998 medicaid settlement with the tobacco companies, & thats not even adjusting for inflation...bank stocks responded favorably, with BofA up 6% on the announcement...

Banks have already set aside reserves to cover their out of pocket expenses, and most of the principal write-downs have already been taken by the banks, who knew going in that these underwater mortgages are worth far less than their nominal value; they now gain immunity from prosecution for servicer related abuses, including document fabrication and foreclosure of homes they had no right to take, no one goes to jail for forgery and they have promised to never do it again...on the other hand, the attorney generals retain the right to pursue civil claims outside of the agreement including securitization fraud and criminal cases; nor does the agreement prevent homeowners or investors from pursuing individual civil cases against the five servicers

...It appears that Schneiderman’s & Biden's lawsuits against MERS will survive, but the nevada & arizona lawsuits against BofA for Countrywide violations of previous consent decrees will be "folded into" the new consent decree...so essentially, the banks are absolved of all crimes against the people; on the other hand, if they defrauded another bank, or investors, they might still be held liable; their rights were the only ones that the administration and the AGs wanted to preserve...our government exists to protect the banks, everything & everyone else is secondary...

You should all recall that congress left last year with a lot of unfinished business regarding routinely renewed tax breaks and only passed a two month extension for unemployment rations, the payroll tax cut, & the "doc fix"...to facilitate coming to an agreement that would last for the rest of the year, a conference committee composed of members of both houses has met several times so far this year in an attempt to hammer out their differences, and they haven't met with much success; although there's been bipartisan agreement to extend the payroll tax cut, they're still encumbered by the ridiculous provision of the debt control act that they must "pay for it", and how to do that is the source of the conflict;

Republicans proposed a package of spending cuts including layoffs & a pay freeze for federal workers, while democrats want a surtax on those earning over a million; for the "doc fix:, which you'll recall would correct the legislated mandate that would cut medicaid doctors reimbursements by 27.4%, the republican rejected a democratic plan to pay for it with savings from war funding; the greatest contention, however has been as to how long to extend rations for the unemployed; while the democrats lean toward cutting 6 weeks from 99 to leave 93 weeks of payments, the republicans would cut as much as 40 weeks, leaving the unemployed with only 59 weeks of assistance, since they're of the belief that only congresscritters should get a check for doing nothing for two years...but even if they extended the unemployment plan now in place, changes they made to the complex eligibility formula when they passed the two month extension will still result in the 32 states that still have the maximum number of weeks gradually having their federal stipends shortened, something that has already happened to the unemployed in michigan, because its jobless rate fell from 11.1 percent at the end of 2010 to 9.3% in december, enough to trigger the state off the extended program...of course, with interest rates for government borrowing effectively negative, they could borrow now at today's rates to pay for these programs, and then pay back less than they borrowed at such time in the future as the economy improves and revenues increased; but understanding that demands that their economic advisers know a little accounting, and as steve roth at angry bear has pointed out, that's not part of their training...

It's been a rather light week for economic reports; probably the most important of those released was for our trade deficit for december (pdf), which came in at a larger than expected deficit of $48.8 billion, up from $47.1 in november...imports of $227.6 billion were far from covering the exports of $178.8 billion, most of which could be accounted for by oil imports averaging over $104 a barrel and a $23 billion trade deficit with china...the report we're going to take a closer look at this week is the december report on consumer credit from the Fed, because the unusual spike of 9.9% we noticed in the november report seems to have started a trend, as december's consumer credit increased at an annual rate of 9.3% over that...remember, these amounts are already seasonally adjusted, so we're not just seeing a normal holiday related jump, we're looking at increases that are at a 9.9% & 9.3% jump above what would have been expected for those months

...Now, this was widely reported as a surge in holiday credit card borrowing, but if you check the Fed report, you'll see that the 9.3% increase resulted from only a 4.1% increase in revolving credit (ie, credit cards) up $2.76 billion, to $800.98 billion, while non revolving credit (cars, yachts, student loans) increased 11.8%, up $16.55 billion, to $1.697 trillion...this is shown clearly in the adjacent chart from zero hedge, which shows revolving credit monthly increases or decreases in blue, and non-revolving credit in red, over the past 5 years...scroll down to the third table in the Fed release, where unadjusted amounts of consumer credit outstanding are reported, and you'll see debt increases by holder; and what stick outs like a sore thumb is consumer debt held by the federal government, which is almost increasing exponentially: $98.4B in 2007 $111.0B in 2008, $186.0B in 2009, $316.4B in 2010, & $425.1B at the end of 2011

...Since this report doesnt include home loans, it's pretty clear we're seeing a spike in borrowing for education...and since approximately the same number of young people are entering college each year, this more than likely is indicative of underemployed adults borrowing to enhance their education, which is exactly what a “credit karma” analysis of student debt found; for those between age 35 and 49 saw their student debt burden increase by 47%..and just this week, the NACBA (National Association of Consumer Bankruptcy Attorneys) warned of a student loan "debt bomb", now nearly a trillion dollars, which cant be discharged thorough bankruptcy, & which they believe could be the next bubble to burst…& btw, that's something else congress has to address, as the interest rate on federal student loans is scheduled to double from 3.4% to 6.8% unless Congress acts before summer...

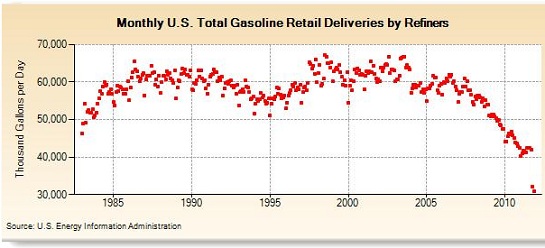

Just one more thing i want to look at, that's been kicking around this week in some of the more obscure corners of the blogosphere...after a reader at Mish's blog noted a significant decline in gasoline consumption, charles hughes smith dug up this adjacent chart of gasoline retail (ie gas station) deliveries per monthly rate from the US EIA; its easy to see how much our gasoline usage has declined during the recession, and as he discusses, there are some obvious reasons; unemployment, more efficient cars, behavior changes, etc...what is of concern is the collapse over the past 2 months; its now down to nearly 30 million gallons a day, which is about half of what was being used early last decade...scanning the 90s, we can see that january is typically an outlier to the downside, but there doesnt appear to be any 2 month precipitous drop anywhere near as severe as we've just seen in the historical record...since there's nothing else in any of the other reports that i've seen that could explain this, i really dont know what to make of it...but it's something we'll have to keep an eye on...

A foreclosure fraud footnote: each state gets a different amount of the mortgage fraud settlement...for instance, ohio gets $335 million, kansas gets $50 million, etc...yves smith has posted a Settlement Breakdown by State Plus Other Official Propaganda; i found the embedded scribd documents difficult to load and navigate; to find out how much your state got its probably easier just to google state name mortgage settlement amount, invariably the amount shows on google without linking to & reading a local article...

links

International Financial News - - - interactive - click on each